The opportunity for a new job or career is an exciting time, and if you are like many Americans, you will likely change jobs or careers more than once. A question we get all the time as advisors is, “what do I do with my old 401(k)?”

You could leave the money in your previous employer’s 401(k) plan. Certain company plans have a minimum balance required to leave your money in their plan. The downside to this idea is now you will have multiple 401(k)s to keep track of.

Another potential issue might arise if your previous employer is bought out or switches 401(k) providers. This now means you will have to spend time tracking down new account information. Research completed by Capitalize shows an estimated 24.3 million 401(k) accounts have been left behind by job changers.

Second option – you could roll your old 401(k) to your new employer’s 401(k) plan. If your new employer plan allows this, it is an easy way to keep track of your retirement savings. Plus, your new 401(k) plan might have better investment options and lower fees. You will want to make sure you complete a direct rollover (rolling funds directly from your old 401(k) to new 401(k) plan) so you avoid taxes or penalties.

Another great (and convenient) option is rolling your old 401k into an IRA (Individual Retirement Account) or Roth IRA. Doing this will broaden the investment options available to you, as you will be in control of your retirement savings and not beholden to the plan’s rules.

If you contributed to the Pre-Tax or Traditional option in your 401(k) you will want to directly roll these dollars over to a Traditional IRA, so you pay taxes only when you take withdrawals. Some employer plans have a Roth 401(k) option, so these dollars can be rolled over to a Roth IRA.

In rare cases folks cash out their old 401(k)s. Withdrawing funds from your 401(k) counts as income to you, and depending on your age or withdrawal reason you may have to pay taxes and penalties on this type of transaction.

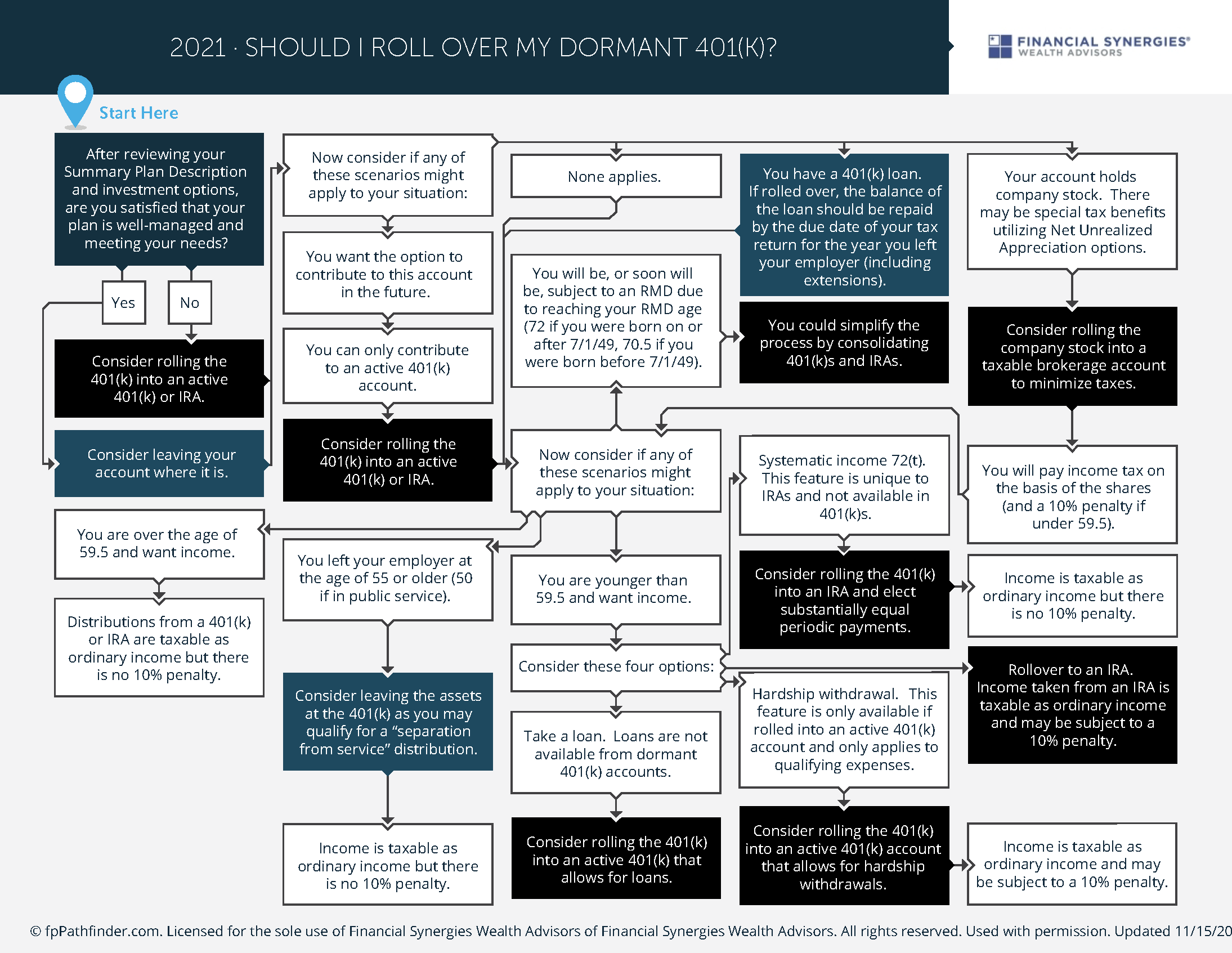

Below I’ve included a great flowchart that illustrates the various old 401(k) options and situations in which they may be utilized. You can also download the flowchart PDF here.

Please visit with your financial advisor before deciding what to do with your old 401(k). We would be more than happy to advise you on the best course of action.