The purpose of this case study is to provide an inside look into how Financial Synergies Wealth Advisors provides trusted financial advisory and wealth management services for our clients. While this is just a sample financial plan, it does provide a real life glimpse into the financial advisor-client relationship. The case study also outlines the various stages new clients go through when working with us.

The opportunity for both parties to get to know one another. The meeting focuses on the Matthews’ questions and financial situation, and the scope of services provided by Financial Synergies Wealth Advisors.

The Matthews and Financial Synergies agree to move forward together with a formalized wealth management agreement and open investment accounts to be managed by the firm.

We review the Matthews' financial situation including goals, concerns, net worth, income, expenses, insurance, estate planning, and taxes.

We present detailed recommendations for the Matthews’ entire financial situation, including a review of our investment philosophy and recommendations.

We outline the next steps and begin the process of putting the financial plan recommendations into motion.

Jeff and Susan Matthews are middle-aged working professionals who have an eye on retirement in the next few years. Jeff is 62 years old and works as a sales consultant for a large industrial company. His wife, Susan, is 57 and is a nurse practitioner. They have two children, Stephen and Mary, who both graduated from college in the last few years.

Jeff and Susan have never engaged in a formal relationship with a financial professional. With their children out of the house, they are beginning to have questions about when they can retire and what that may look like. In the past, their discussions on retirement were brief because it seemed so far off and was very overwhelming.

Things changed when Jeff’s company recently announced upcoming layoffs. He was notified that he would be receiving a mandatory retirement package. He was caught off guard by the decision because he has only worked for the company for a few years. He had pondered retirement but did not expect this change so suddenly. As part of his retirement package, Jeff will receive:

Given this unexpected change, they decided to research financial firms and quickly realized the importance of working with a CFP® professional. They read several articles about the qualifications to seek in a financial advisory firm – most importantly a fee-only, fiduciary advisor. These professionals are not compensated by selling financial products and they are required to put the best interests of their clients first.

Their online search led them to the website for Financial Synergies Wealth Advisors (FSWA). Reading about their many years of service and their expertise working with retirees, Jeff and Susan felt comfortable contacting the FSWA team.

Shortly after their initial inquiry with Financial Synergies, they were contacted by one of the firm’s financial advisors. Jeff and Susan briefly explained their situation and how they were interested in discussing more about their circumstances. Jeff’s employment termination would be effective in 60 days, so they needed help.

The FSWA advisor welcomed the opportunity to meet with Jeff and Susan. He set clear expectations for this “discovery” meeting. The purpose was to better understand their financial situation and learn more about their goals for the future. The advisor assured them that there was no obligation when meeting with the team. The ultimate purpose is to determine if FSWA is a good fit for their needs and to make sure the team could add value to their financial lives.

During the discovery meeting, Jeff and Susan and the Financial Synergies advisors had a detailed conversation about their family, their finances, and their careers. They asked a lot of questions that Jeff and Susan had not considered before. The advisors spent time asking how they felt about retirement, what concerns they had, their experience with money throughout their life, and what goals they had for this next chapter of their lives.

The advisors provided a background on the firm and important details about their services, including:

Assisting clients for over 35 years.

Fee-only, fiduciary advisors who put the client’s best interests first.

Wealth management services including investment management and financial planning.

Client’s money is held at third-party custodians to provide more security and transparency.

Clear explanation of costs & fees.

Recognized as a top wealth management firm.

Given that retirement was not too far off for Jeff and Susan, the advisors explained their retirement income distribution strategy. Known as “The Retirement Salary,” the advisors walked them through the detailed process of how they provide ongoing, flexible income to their retiree clients.

It is a great complement to their overall investment strategy, and the advisors emphasized they do not use any investment products – like annuities – for retirement income. Jeff and Susan felt assured that when they were ready to fully retire, the FSWA team knew what to do.

Financial Synergies even has a program called Pathway to help young professionals like their children. They wished they had the opportunity to work with a great team like this early on in their careers.

Overall, Jeff and Susan found the discovery meeting very refreshing and they learned a lot about Financial Synergies’ wealth management approach. The advisors emphasized the importance of adding value to clients’ lives and the team felt they could certainly do so for Jeff and Susan. They left the meeting with the understanding that the FSWA team would follow up in the agreed upon time frame regarding their decision.

Jeff and Susan felt confident that the CFP® professionals at Financial Synergies could help as they faced a major lifestyle shift. Having mutually agreed to work together, Jeff and Susan met with the advisor team to complete the paperwork and formalize the relationship. They signed the non-binding management agreement and were given other important disclosures and privacy documents.

Prior to the meeting, Jeff and Susan were provided a digital questionnaire that gathered their personal and financial information. The team prepared the necessary paperwork to set up the needed investment accounts (such as IRA, Roth IRA, brokerage accounts, trusts, etc.) at the desired custodian (Schwab or Fidelity) and explained the transition process, which made it seamless and easy.

The FSWA team laid out a clear time frame for the accounts to transfer. They reviewed the digital tools they use for secure document sharing & storage and the online portals Jeff and Susan will access to review their investment account performance and financial plans. Jeff and Susan were impressed with the technology Financial Synergies provides to their clients. While they were able to meet in-person, it was clear to Jeff and Susan that FSWA has the capabilities to work with clients regardless of where they live.

Financial Synergies offers multiple client portals for investment management and financial planning.

Jeff and Susan next met with the FSWA team for a detailed fact-finding meeting. The advisors explained how they like to do a “deep dive” into all aspects of their financial lives. While Financial Synergies will eventually manage a majority of their investment accounts, there are other important factors that need to be incorporated into the plan. During the conversation, the FSWA team learned the following with regard to Jeff and Susan’s current financial situation:

Jeff’s current 401k balance is $100,000 (pre-tax) and he’s fully vested in the company’s matching contributions.

Jeff has an old 401k plan from his last job worth $600,000 (pre-tax).

He also has a pension from his old employer worth $150,000 (lump sum, pre-tax).

Jeff’s current company RSU balance is $60,000 ($30,000 vested / $30,000 unvested).

Susan contributes 10% to her 403b plan at the hospital and has a $450,000 balance.

The hospital makes a 6% annual contribution on her behalf in a separate profit-sharing plan, which is worth $60,000 (pre-tax).

Jeff and Susan purchased an annuity when they were younger for $50,000 and its current value is $75,000.

They have $200,000 in cash between their checking and savings account.

Jeff and Susan purchased their current home 10 years ago; they paid $300,000 and owe $150,000 on the mortgage (4% interest rate, 30-year term). The current value is $360k.

Jeff drives a company vehicle, so he does not have a car loan.

Susan leases an SUV for $400/month and typically likes trading it in every three years.

Outside of the mortgage, they do not have any other debts.

Jeff’s salary was $150,000 and his annual bonus was $25,000.

Susan’s income is $95,000 per year.

They are both fully qualified for Social Security. Jeff’s benefit is projected to be $3,100 at his Full Retirement Age and Susan’s benefit is estimated to be $2,500/month.

Jeff and Susan spend $6,000/month for day-to-day expenses (gas, groceries, utilities, etc.).

The mortgage payment is $1,145/month.

They like to travel and typically spend $12,000/year on family vacations.

They each purchased 20-year term policies when their children were young; the death benefit is $500k each and total premiums of $1,200/year. There are 4 years remaining on each policy, with the option to renew.

They purchased long-term care insurance a few years ago and pay $300/month for each policy.

Jeff and Susan each set up a basic will when their children were young. However, they do not have any powers of attorney (POAs) for health and finances.

They would like to leave something for their children but don’t have specific inheritance goals. Both of their parents are still alive and are in decent financial shape. If they were to have a significant health event, it could strain their finances.

Jeff wants to start his own consulting business and possibly retire by age 65. He may work longer if the business is doing well and he enjoys it.

Susan would like to retire at 60. Susan would like to do more traveling when they retire. Jeff would prefer to buy a lake house. Jeff will need to purchase a vehicle.

Jeff and Susan have concerns about running out of money in retirement.

They are concerned about the cost of healthcare in retirement.

They don’t want to be a burden for their children as they get older.

Jeff hates debt and wants to pay off the home loan. Susan is more comfortable paying off the mortgage over time, which can be a source of frustration for them.

They are holding more cash than they need but are unsure of what to do with it.

Jeff is planning to start his Social Security benefits early at age 62.

Jeff, Susan, and the Financial Synergies team met to review the financial plan recommendations. They recapped the information gathered in the fact-finding meeting. The advisors had input this information into their financial planning software and reviewed all aspects of the plan.

The advisors walked them through a mathematical technique called a Monte Carlo analysis. It is a simulation that takes their finances and helps model the outcomes when investing in different market cycles (it helps determine whether or not they will run out of money). The current situation resulted in a 56% success rate.

While the current projections seemed dire to Jeff and Susan, the advisor team saw several areas where they could improve. They made a wide range of recommendations, including:

They recommended Jeff pursue his consulting business. Jeff thinks he could easily earn $75,000 based upon his industry experience and contacts. This will avoid the need to pull from the portfolio in the short-term.

Reduce their travel budget from $12,000 to $8,000 in the near-term while Jeff launches his consulting business.

Delay Jeff’s Social Security until age 70 to maximize his benefit.

Enroll in Medicare when they each reach age 65 when the retiree health benefits expire. Enrolling on time will prevent paying future permanent penalties.

Keep $100,000 of cash for an emergency fund and to help cover the startup costs of Jeff’s business.

Do not have Jeff file for Social Security early at age 62. This will result in a permanent benefit reduction and may subject him to the annual Earnings Limit test.

Have Susan start her benefit at her Full Retirement Age (67).

Jeff should work with his CPA to set up the proper entity for his consulting business. He can deduct several business expenses, including his new vehicle.

Jeff should make tax deductible contributions to his IRA. As his income increases, consider setting up a solo 401k to maximize investment & tax savings.

Consider making Roth conversions from retirement accounts. This may help reduce taxes in retirement and provides the opportunity for investments to grow tax-free.

The advisor team provided a referral to a qualified CPA firm.

Do not renew the term life insurance policies; the need for insurance is low with children being financially independent, and the premium costs on new policies at their age are too high.

Maintain the current LTC insurance policies to offset potential healthcare costs in the future. If the premium costs increase in the future, they may consider adjusting the benefits to lower premium costs (if needed).

Purchase an umbrella liability policy to go along with their homeowners & auto insurance policies.

The advisor team provided a referral to a qualified insurance firm.

Meet with an estate attorney to update wills and set up the necessary POAs. Also, update all beneficiary information on the retirement accounts and annuities.

Confirm all retirement accounts have the correct, updated beneficiary information.

Financial Synergies provided a referral to a qualified estate planning firm.

Roll Jeff’s current 401k, old 401k, and pension lump sum into a rollover IRA. This helps consolidate his investments and reinvest into a diversified portfolio.

Transfer the vested company stock into a joint brokerage account. Sell the stock immediately and reinvest into a diversified portfolio.

Transfer the cash for their emergency fund to a high-yield savings account that pays a higher interest rate and is FDIC insured.

Invest the remaining cash into a diversified portfolio in a joint brokerage account ($100k).

Transfer their existing annuity to a lower cost annuity option via a tax-free 1035 exchange. This will reduce the internal fees for the annuity and improve the investment options.

Roll over Susan’s 403b and profit-sharing plan when she retires for better investment options and to consolidate accounts.

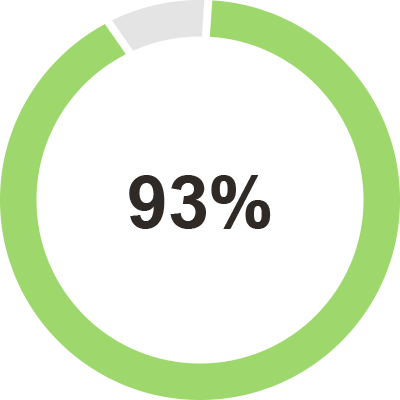

The advisors were able to show Jeff and Susan how these changes would impact them. By implementing these recommendations, the Monte Carlo results increased dramatically to 93%.

Probability of Success

Probability of Success

Jeff and Susan were very pleased throughout the entire process with Financial Synergies. They would have felt overwhelmed with all the decisions to make and the advisor team helped them avoid several pitfalls that could have been costly. They feel that the team understands their situation very well, and they have laid out a clear plan moving forward.

The advisor team explained what would happen over the next several months. Jeff and Susan will receive quarterly performance reports from Financial Synergies. They will monitor the investment accounts on an ongoing basis and make any rebalancing adjustments as needed. The team set reminders for important dates upcoming, such as Jeff’s employment termination, rolling over the retirement accounts, and coordinating with the CPA on tax materials. They also provided an estate attorney recommendation and helped coordinate a meeting to complete their estate documents.

The advisor team planned a follow up meeting later in the year, and asked Jeff and Susan about the frequency they would like to meet each year going forward. Jeff and Susan did not foresee the major life changes that came their way. It was overwhelming and scary, but they felt very fortunate about their decision to work with Financial Synergies. They feel confident that they’re working with the right team that can help make their future retirement dreams a reality.

Disclaimers

This is a hypothetical illustration of the services provided by Financial Synergies Wealth Advisors. Investing involves risk, and past performance is not a guarantee of future results. None of the information conveyed in this example should be considered financial advice.

4400 Post Oak Pkwy #200

Houston, TX 77027

Financial Synergies Wealth Advisors is a fee-only, fiduciary Financial Advisor in Houston, Texas. We specialize in wealth management services, including comprehensive financial planning and investment management.

For more than thirty years we’ve been serving the financial needs of individuals, families, and businesses in Houston, Texas and around the country.

Wealth Management Services include financial planning, retirement planning, investment management, tax planning, insurance planning, estate planning, and company retirement plans.

Find out if we’re a good match for your financial planning and investment management needs. We offer a free, no-obligation consultation to help us get to know each other. We can meet by phone, in-person, or online.

Financial Advisor Houston, TX

4400 Post Oak Pkwy #200Houston, TX 77027

4400 Post Oak Pkwy #200

Houston, TX 77027

Financial Synergies Wealth Advisors is a fee-only, fiduciary Financial Advisor in Houston, Texas. We specialize in wealth management services, including comprehensive financial planning and investment management.

For more than thirty years we’ve been serving the financial needs of individuals, families, and businesses in Houston, Texas and around the country.

Wealth Management Services include financial planning, retirement planning, investment management, tax planning, insurance planning, estate planning, and company retirement plans.