Despite the jump in interest rates this year, the yields on many corporate bonds remain low. This is driven by many of the same factors that continue to push the stock market higher: the strong economic recovery and rebound in corporate profits. Last week’s blowout jobs report, for instance, showed that 916,000 jobs were added in March and the unemployment rate fell to only 6%. While this is great news in general, it makes it even more challenging for investors to generate sufficient portfolio income.

This is because there are two major factors that determine corporate bond yields. The first is the level of interest rates in the economy, usually measured by U.S. Treasury yields. These have risen significantly this year as the economy has recovered but are still near historic lows compared to the past several decades. For example, the 10-year Treasury yield, after more than tripling from its lowest point one year ago to 1.7%, is still well below the 2008 low of 2.1%.

And while higher yields are positive for investors going forward, rapidly rising rates can be problematic for existing bond holdings – a challenge known as duration risk. At the moment, the U.S. Aggregate bond index is down 3.1% for the year. This is similar to 2013 when interest rates rose swiftly during the Fed “taper tantrum” – the last time the index was negative on a calendar year basis.

The second and perhaps more important factor today is credit risk. This measures and compensates investors for the riskiness of a bond issuer above and beyond Treasuries. When interest rates are extremely low, credit risk can play a much larger role in providing sufficient income, as was the case over the last business cycle. Also in 2013, for instance, high yield bonds returned 7.4% even as Treasury bond prices fell.

It’s due to the combination of these two factors that corporate bond yields are low: although interest rates are rising, spreads continue to compress as the economy improves and the outlook for corporate profitability brightens. After all, if companies are more likely to pay their bondholders on time, the level of yield that investors need to compensate for risk is lower – even for the most speculative issues. At the moment, the spreads on high yield bonds are near their lowest levels since the mid 2000’s.

Unfortunately, there are still no easy answers for generating sufficient yield. This will continue to depend on individual goals and portfolios – one key reason that investors can benefit from proper financial advice and guidance.

Just as they have since 2008, investors need to weigh credit and duration risk relative to the rest of their portfolios. We must consider alternative sources of yield, whether in other sectors / regions of fixed income, and taking a total return approach.

Ultimately, staying diversified and focusing on broader objectives, rather than just income, is most likely the best approach for investors with longer time horizons. Below are three charts that highlight the challenges investors face today in generating portfolio income.

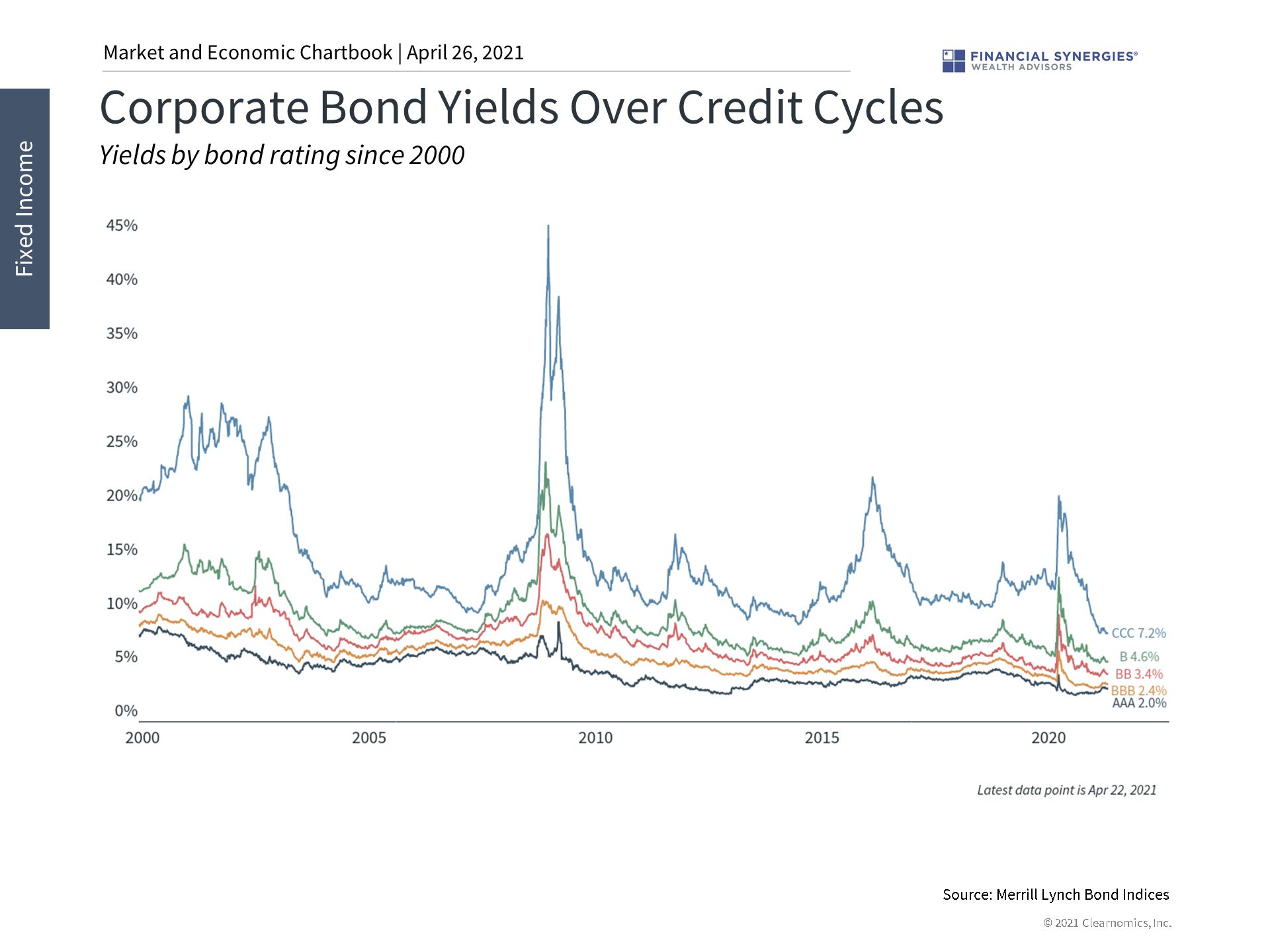

1. Corporate bond yields remain low even as interest rates rise

Credit spreads continue to collapse as the economy recovers and profitability improves. Although this has boosted returns for more speculative parts of fixed income, this has also amplified the challenge of generating yield.

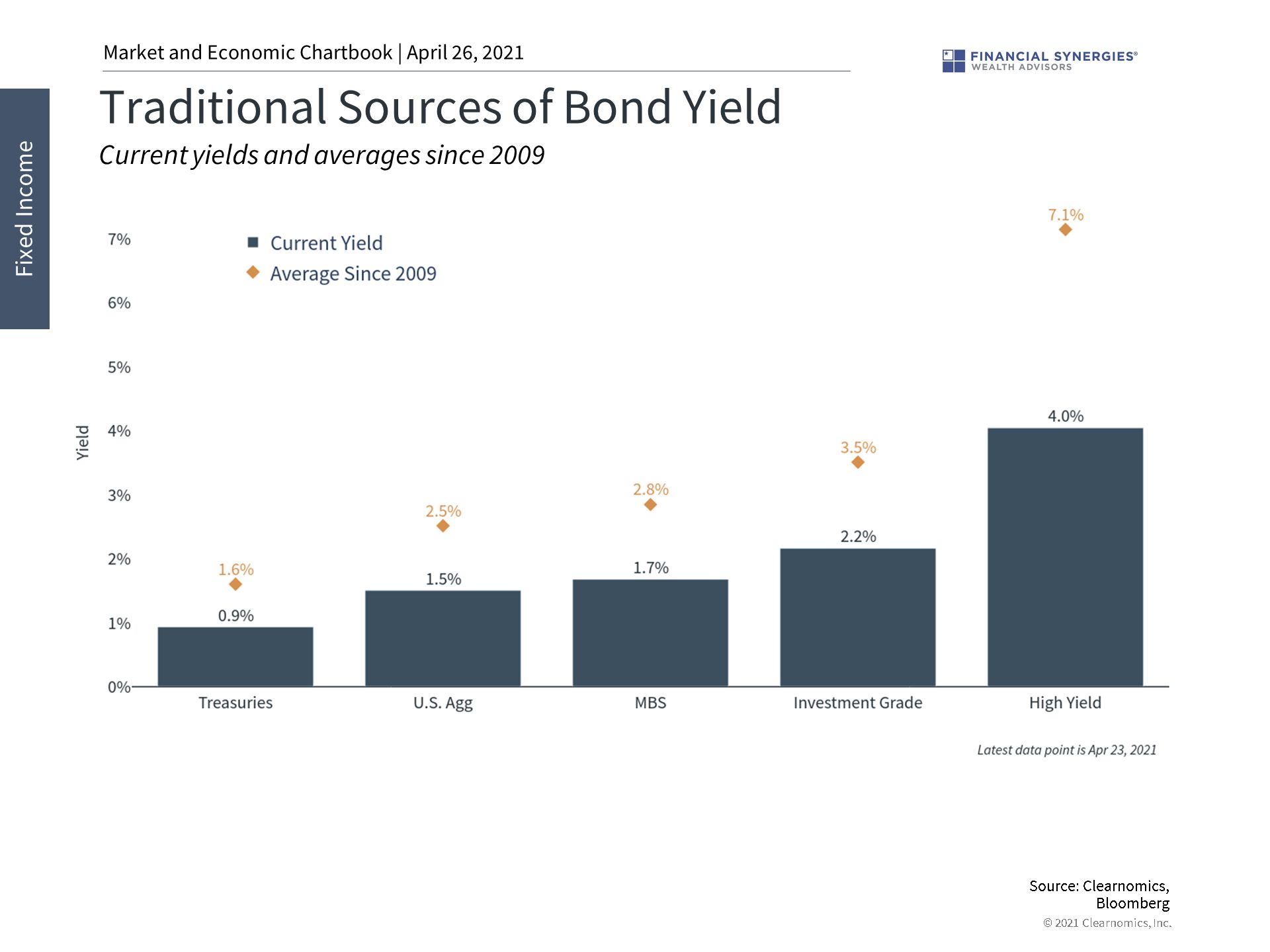

2. Yields are much lower today than over the past cycle

There are no simple answers today with traditional sources of bond yield at much lower levels. The chart above compares today’s yields to averages since 2009 which was already a low-yielding environment.

3. A more diversified approach may be needed

Investors may need to broaden their search when considering sources of yield. They may also need to broaden their approach and focus on diversification and total return rather than just income.

Source: Briefing Investor

Why Investors Still Face Low-Yield Challenges

Despite the jump in interest rates this year, the yields on many corporate bonds remain low. This is driven by many of the same factors that continue to push the stock market higher: the strong economic recovery and rebound in corporate profits. Last week’s blowout jobs report, for instance, showed that 916,000 jobs were added in March and the unemployment rate fell to only 6%. While this is great news in general, it makes it even more challenging for investors to generate sufficient portfolio income.

This is because there are two major factors that determine corporate bond yields. The first is the level of interest rates in the economy, usually measured by U.S. Treasury yields. These have risen significantly this year as the economy has recovered but are still near historic lows compared to the past several decades. For example, the 10-year Treasury yield, after more than tripling from its lowest point one year ago to 1.7%, is still well below the 2008 low of 2.1%.

And while higher yields are positive for investors going forward, rapidly rising rates can be problematic for existing bond holdings – a challenge known as duration risk. At the moment, the U.S. Aggregate bond index is down 3.1% for the year. This is similar to 2013 when interest rates rose swiftly during the Fed “taper tantrum” – the last time the index was negative on a calendar year basis.

The second and perhaps more important factor today is credit risk. This measures and compensates investors for the riskiness of a bond issuer above and beyond Treasuries. When interest rates are extremely low, credit risk can play a much larger role in providing sufficient income, as was the case over the last business cycle. Also in 2013, for instance, high yield bonds returned 7.4% even as Treasury bond prices fell.

It’s due to the combination of these two factors that corporate bond yields are low: although interest rates are rising, spreads continue to compress as the economy improves and the outlook for corporate profitability brightens. After all, if companies are more likely to pay their bondholders on time, the level of yield that investors need to compensate for risk is lower – even for the most speculative issues. At the moment, the spreads on high yield bonds are near their lowest levels since the mid 2000’s.

Unfortunately, there are still no easy answers for generating sufficient yield. This will continue to depend on individual goals and portfolios – one key reason that investors can benefit from proper financial advice and guidance.

Just as they have since 2008, investors need to weigh credit and duration risk relative to the rest of their portfolios. We must consider alternative sources of yield, whether in other sectors / regions of fixed income, and taking a total return approach.

Ultimately, staying diversified and focusing on broader objectives, rather than just income, is most likely the best approach for investors with longer time horizons. Below are three charts that highlight the challenges investors face today in generating portfolio income.

1. Corporate bond yields remain low even as interest rates rise

Credit spreads continue to collapse as the economy recovers and profitability improves. Although this has boosted returns for more speculative parts of fixed income, this has also amplified the challenge of generating yield.

2. Yields are much lower today than over the past cycle

There are no simple answers today with traditional sources of bond yield at much lower levels. The chart above compares today’s yields to averages since 2009 which was already a low-yielding environment.

3. A more diversified approach may be needed

Investors may need to broaden their search when considering sources of yield. They may also need to broaden their approach and focus on diversification and total return rather than just income.

Source: Briefing Investor

Recent Posts

Your “Magic” Retirement Number?

The Market Pullback, Geopolitical Risks, Inflation, and More

Week in Perspective: Stocks Startled by Inflation, Conflict [Apr. 15-2024] – VIDEO

Subscribe to Our Blog

Shareholder | Chief Investment Officer