3rd Quarter 2022 Market Review and Commentary

Please find below our quarterly market review and commentary for the 3rd Quarter of 2022. We hope you find it helpful.

If you would like a PDF copy of this report to download or share with friends, please find it here: 3rd Quarter Market Review and Commentary – Oct 2022 (PDF)

Also, you can download a PDF copy of my disclosures and supporting charts/graphs by clicking here.

A Still-Hawkish Fed and Growing Geopolitical Risks Offset a Likely Peak in Inflation to Pressure Stocks in the 3rd Quarter

Global markets declined again in the third quarter as inflation remained near multi-decade highs, geopolitical tensions escalated further, and the Federal Reserve continued to aggressively hike interest rates signaling future rate increases will be larger than previously expected.

The third quarter started with a solid rebound in stocks and bonds that was driven by resilient corporate earnings, signs of a possible peak in inflation, and hints from the Federal Reserve that the end of the rate hiking cycle may come sooner than markets initially expected.

Starting with earnings, corporate results for the second quarter were much better than feared. Despite high inflation and lingering supply chain issues, the majority of Q2 earnings reports beat estimates, and that solid performance by corporate America showed investors that, despite numerous macroeconomic challenges, U.S. earnings were holding up much better than expected.

On inflation, several survey-based economic reports showed price declines in June and offered hope that inflation pressures were peaking. Finally, in late July the Federal Reserve raised interest rates by another 75 basis points, but at the press conference Fed Chair Powell stated that, at some point in the future, it’d be necessary for the Fed to slow the pace of interest rate increases. Investors interpreted that comment as a signal that the end of the rate hike cycle may be closer than previously thought.

Hope for a less-aggressive Fed paired with resilient earnings and a possible peak in inflation fueled a 9.2% gain in the S&P 500 in July, its best monthly return since November 2020.

Stocks continued higher through the first half of August, driven by more proof of a peak in inflation and the growing hope that the Federal Reserve would soon “pivot” to a less-aggressive policy stance. Specifically, the July CPI report (released in August) showed clear moderation in price pressures, further entrenching the idea that inflation had peaked.

Investors welcomed this news and confirmation of a peak in inflation, combined with the aforementioned hope of a “Fed pivot,” pushed the S&P 500 to nearly four-month highs by mid-August.

But ultimately, the move higher in July and early August was nothing more than a “Bear Market Rally” as in late August, while making remarks at the Jackson Hole Economic Symposium, Fed Chair Powell dismissed the idea of a looming Fed pivot to less-aggressive policy, dashing hopes that the end of the rate hike cycle was in sight.

Additionally, Powell warned that the U.S. economy will likely feel some “pain” from the Fed’s actions. The reiteration of aggressive policy and historically large rate hikes combined with the warning of looming economic pain hit stocks late in the month, and the S&P 500 gave back all the early August gains to end the month solidly lower, down 4%.

The selling continued in September, as the August CPI report (released in September) showed a slight increase in prices, implying that while inflation pressures had potentially peaked, inflation was not rapidly declining towards the Fed’s target (meaning rates would likely stay high for the foreseeable future).

Then, at the September FOMC meeting, the Federal Reserve again hiked interest rates by 75 basis points and signaled rates will continue to rise to levels higher than previously expected.

Geopolitical concerns also pressured stocks in September as Russia escalated the war in Ukraine by holding referendums in occupied Ukrainian territory, and by announcing a 300,000-person “mobilization” from the general Russian population.

Finally, during the last few days of the month, global currency and bond markets saw a dramatic increase in volatility, as the government of the United Kingdom announced a spending package designed to stimulate the economy. But that would also likely add to inflation pressures and the announcement resulted in a spike in global bond yields while the pound collapsed to an all-time low vs. the dollar, adding to general macroeconomic volatility.

The combination of sticky inflation, expectations of numerous future Fed rate hikes, rising geopolitical tensions, and currency and bond market volatility weighed heavily on stocks and bonds into the end of September, as both markets finished the quarter near the lows for the year.

In sum, the third quarter started with optimism surrounding a resilient corporate earnings outlook, a potential peak in inflation, and a closer-than-expected end to the current Fed rate hiking cycle. But throughout August and September that optimism was eroded by sticky inflation data and a more hawkish-than-expected Federal Reserve.

As we start the fourth quarter markets remain in search of concrete positive catalysts that signal declining inflation pressures and a less-aggressive Federal Reserve.

Third Quarter Performance Review

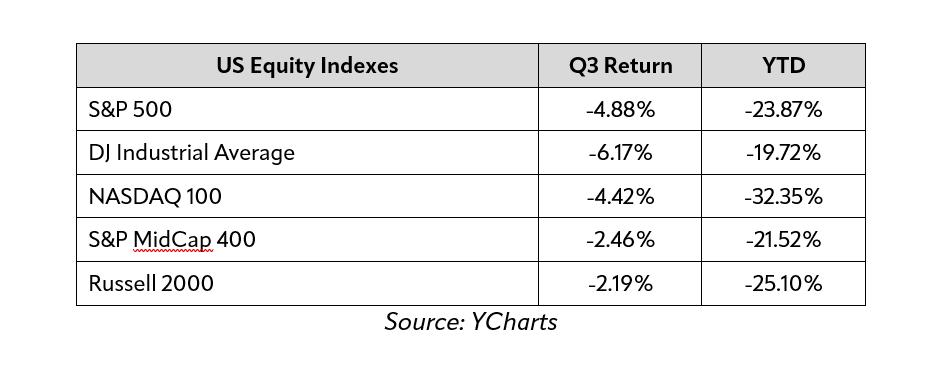

All four major stock indices posted negative returns for the third consecutive quarter, although unlike the first two quarters of 2022, the tech-heavy Nasdaq did not badly lag other indices and the quarterly declines were fairly uniform across the most widely followed U.S. equity indexes.

By market capitalization, small-cap stocks outperformed large-cap stocks for the first time this year, although the performance gap was modest. Small-cap outperformance came mostly from gains early in the third quarter as markets broadly rallied on hopes of a quick decline in inflation and a sooner-than-expected Fed pivot. But as those hopes faded in late August and September and interest rates hit new highs, investors rotated back to the perceived safety of large-cap stocks, diminishing the performance gap between small and large-caps significantly.

From an investment style standpoint, both value and growth registered losses for the second straight quarter. However, unlike the first half of 2022, growth relatively outperformed value in the third quarter. Growth enjoyed a strong rebound early in the quarter, again as markets rallied on the hope of peak inflation and a Fed pivot that would signal a peak in interest rates. However, that growth outperformance shrank late in the quarter as inflation remained high and the Fed signaled there was no imminent end to the rate hiking cycle.

On a sector level, just one of the 11 S&P 500 sectors finished the third quarter with a positive return. Consumer discretionary posted a positive return thanks to strong consumer spending and still-low unemployment. The energy sector, meanwhile, finished the quarter with a fractional loss as energy stocks benefitted from solid earnings and strength in natural gas prices. More broadly, traditionally defensive sectors relatively outperformed over the past three months, as investors positioned for slower future economic growth.

Sector laggards in the quarter included communication services, real estate, and materials. Communication services have lagged throughout 2022 as investors shunned expensively valued tech companies. Real estate, meanwhile, declined in the face of spiking mortgage rates and as home price appreciation began to slow.

Finally, the materials sector traded lower following earnings warnings from multiple chemical companies and a sharp drop in certain commodities prices in the third quarter, which was driven by a stronger dollar and growing worries about the global economy.

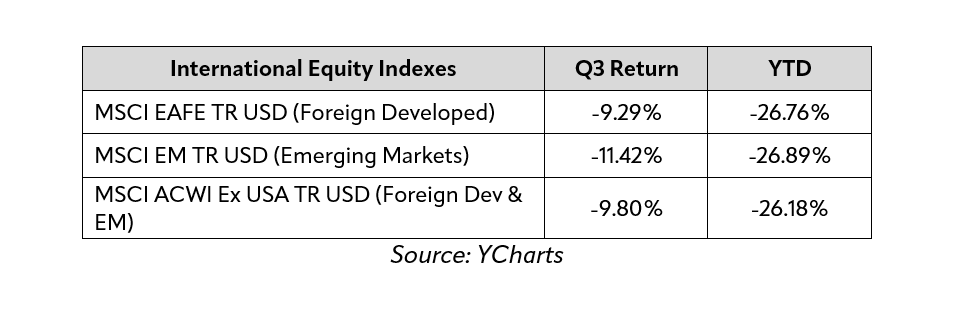

Internationally, foreign markets badly underperformed U.S. markets during the third quarter, as surging electricity prices in Europe and the U.K., interest rate hikes by the European Central Bank and Bank of England, and lasting geopolitical risks weighed heavily on foreign developed markets. Emerging markets, meanwhile, underperformed both foreign developed markets and U.S. markets as a surging U.S. dollar offset hopes for a continued economic reopening in China.

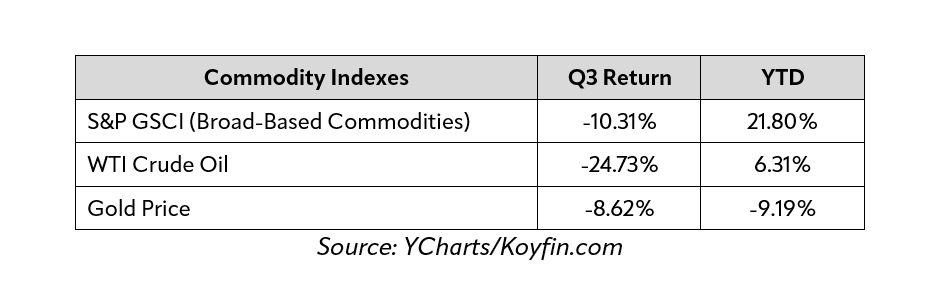

Commodities dropped sharply in the third quarter as a combination of a multi-decade high in the U.S. dollar, growing fears of a global recession, and sharply rising real interest rates weighed on industrial commodities as well as traditional safe havens like precious metals. Oil prices fell in the quarter as concerns about future demand offset geopolitically based worries about supply. Gold, meanwhile, logged solidly negative returns for the second straight quarter thanks to rapidly rising real yields, the surging dollar, and fading market-based inflation expectations.

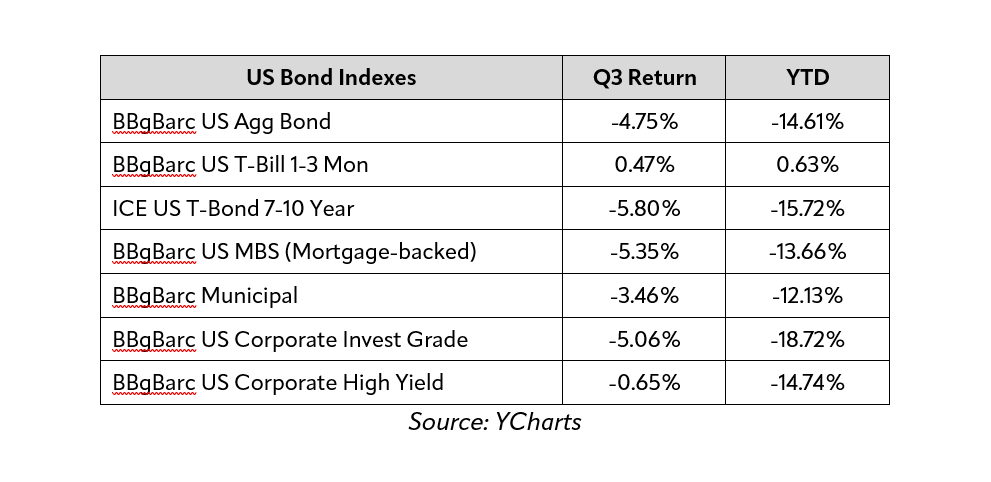

Switching to fixed-income markets, most bond indices posted solidly negative returns for the third straight quarter. Stubbornly elevated inflation, continued Fed rate hikes, and a late-quarter selloff in global sovereign bonds (driven by the ill-conceived fiscal spending package from the United Kingdom) saw most bond classes end the third quarter lower, extending the year-to-date declines.

Looking deeper into the bond markets, as has been the case all year, shorter-term Treasury Bills outperformed longer-duration Treasury Notes and Bonds as the threat of greater than previously expected Fed rate hikes and still-high inflation weighed on fixed income products with longer durations. For the second straight quarter, short-term Treasury Bills finished the quarter with a slightly positive return.

Corporate bonds relatively outperformed longer-duration government bonds in the third quarter thanks mostly to still-solid U.S. economic data. Higher yielding, lower quality corporate debt declined less than investment grade corporate bonds as resilient corporate earnings kept default risks generally low.

Fourth Quarter Market Outlook

As we start the final quarter of 2022, an honest assessment of the macroeconomic landscape reveals that the markets and the economy are still facing numerous challenges from still-high inflation, ongoing Fed rate hikes, and geopolitical instability.

Valuations on many quality companies are quickly approaching pre-pandemic levels, while the S&P 500 more broadly is trading at a valuation that has, historically speaking, been attractive over the longer term.

But while the outlook for risk assets remains challenged, that reality must be considered in the context of a market that has declined substantially and, presumably, already priced in a lot of “bad news.” Valuations on many quality companies are quickly approaching pre-pandemic levels, while the S&P 500 more broadly is trading at a valuation that has, historically speaking, been attractive over the longer term.

Additionally, multiple sentiment indicators have hit or are approaching levels that historically have represented extreme pessimism and bearishness, and they are largely ignoring the reality that there has been some improvement in the macroeconomic outlook over the past several months.

First, inflation has likely peaked. Multiple inflation indicators are showing a peak and decline in price pressures, and while the Consumer Price Index remains far above the Fed’s target of 2%, any swift deceleration in inflation would likely be a material positive catalyst for both stocks and bonds.

Second, the less-aggressive Fed pivot will still occur, perhaps as early as the fourth quarter. According to the Fed’s estimates, interest rate increases will begin to slow in the coming months, and the last rate hike for this cycle could occur in March 2023 or sooner. If that turns out to be the case, and the Fed signals to markets that this rate hike cycle is approaching its end, that will likely be a materially positive catalyst for both stocks and bonds, and that’s evidenced by the July and August rallies that were driven by hopes of a less-aggressive Fed.

Third, geopolitical tensions remain very elevated as Russia has recently escalated the war in Ukraine and the risk of a broader conflict simply can’t be ruled out. But most Western countries remain united in their opposition to the Russian invasion of Ukraine and that will continue to be a powerful deterrent to Russian President Putin.

Additionally, even some of Russia’s most important allies, including China and India, have voiced concerns about the escalation of the war over the past month which has further isolated Russia from the global community. Any reduction in geopolitical tensions would provide a surprise boost for global risk assets, including U.S. stocks and bonds.

Finally, amidst a difficult macroeconomic backdrop, the U.S. economy and corporate America have proven impressively resilient. Most measures of U.S. economic growth remain in solid shape, while U.S. corporate earnings estimates have stayed largely elevated, and the widespread earnings declines that were feared back in early 2022 simply have not materialized.

Bottom line, the outlook for markets and the economy remains challenged, but investors have again priced in a lot of “bad” news already, with valuations now at levels that are historically attractive.

Additionally, according to some indicators, sentiment is as pessimistic as it was during the depths of the financial crisis, and if inflation suddenly decelerates quickly, the Fed signals a clear end to rate hikes, or there’s positive geopolitical news, the potential is there for a powerful rally in both stocks and bonds.

This is a difficult market and a complicated moment for the world, but history is clear: Positive surprises can and have occurred even in difficult times such as this, and through periods of similar macroeconomic turmoil, markets eventually recouped the losses and moved to meaningful new highs. There is no reason to think this time will be any different.

We understand the risks facing both the markets and the economy, and we are committed to helping you effectively navigate this challenging investment environment. Successful investing is a marathon, not a sprint, and even extended bouts of volatility like we’ve experienced so far this year are unlikely to alter a diversified approach set up to meet your long-term investment goals.

As always, we will remain patient and stick to the long-term plan, as we’ve worked with you to establish a unique, personal allocation target based on your financial position, risk tolerance, and investment timeline.

Rest assured that our entire team will remain dedicated to helping you successfully navigate this market environment.

Please do not hesitate to contact us with any questions, comments, or to schedule a portfolio/financial plan review.

Sincerely,

Mike Minter, CFP®, CFS®

Senior Portfolio Manager

3rd Quarter 2022 Market Review and Commentary

3rd Quarter 2022 Market Review and Commentary

Please find below our quarterly market review and commentary for the 3rd Quarter of 2022. We hope you find it helpful.

If you would like a PDF copy of this report to download or share with friends, please find it here: 3rd Quarter Market Review and Commentary – Oct 2022 (PDF)

Also, you can download a PDF copy of my disclosures and supporting charts/graphs by clicking here.

A Still-Hawkish Fed and Growing Geopolitical Risks Offset a Likely Peak in Inflation to Pressure Stocks in the 3rd Quarter

Global markets declined again in the third quarter as inflation remained near multi-decade highs, geopolitical tensions escalated further, and the Federal Reserve continued to aggressively hike interest rates signaling future rate increases will be larger than previously expected.

The third quarter started with a solid rebound in stocks and bonds that was driven by resilient corporate earnings, signs of a possible peak in inflation, and hints from the Federal Reserve that the end of the rate hiking cycle may come sooner than markets initially expected.

Starting with earnings, corporate results for the second quarter were much better than feared. Despite high inflation and lingering supply chain issues, the majority of Q2 earnings reports beat estimates, and that solid performance by corporate America showed investors that, despite numerous macroeconomic challenges, U.S. earnings were holding up much better than expected.

On inflation, several survey-based economic reports showed price declines in June and offered hope that inflation pressures were peaking. Finally, in late July the Federal Reserve raised interest rates by another 75 basis points, but at the press conference Fed Chair Powell stated that, at some point in the future, it’d be necessary for the Fed to slow the pace of interest rate increases. Investors interpreted that comment as a signal that the end of the rate hike cycle may be closer than previously thought.

Hope for a less-aggressive Fed paired with resilient earnings and a possible peak in inflation fueled a 9.2% gain in the S&P 500 in July, its best monthly return since November 2020.

Stocks continued higher through the first half of August, driven by more proof of a peak in inflation and the growing hope that the Federal Reserve would soon “pivot” to a less-aggressive policy stance. Specifically, the July CPI report (released in August) showed clear moderation in price pressures, further entrenching the idea that inflation had peaked.

Investors welcomed this news and confirmation of a peak in inflation, combined with the aforementioned hope of a “Fed pivot,” pushed the S&P 500 to nearly four-month highs by mid-August.

But ultimately, the move higher in July and early August was nothing more than a “Bear Market Rally” as in late August, while making remarks at the Jackson Hole Economic Symposium, Fed Chair Powell dismissed the idea of a looming Fed pivot to less-aggressive policy, dashing hopes that the end of the rate hike cycle was in sight.

Additionally, Powell warned that the U.S. economy will likely feel some “pain” from the Fed’s actions. The reiteration of aggressive policy and historically large rate hikes combined with the warning of looming economic pain hit stocks late in the month, and the S&P 500 gave back all the early August gains to end the month solidly lower, down 4%.

The selling continued in September, as the August CPI report (released in September) showed a slight increase in prices, implying that while inflation pressures had potentially peaked, inflation was not rapidly declining towards the Fed’s target (meaning rates would likely stay high for the foreseeable future).

Then, at the September FOMC meeting, the Federal Reserve again hiked interest rates by 75 basis points and signaled rates will continue to rise to levels higher than previously expected.

Geopolitical concerns also pressured stocks in September as Russia escalated the war in Ukraine by holding referendums in occupied Ukrainian territory, and by announcing a 300,000-person “mobilization” from the general Russian population.

Finally, during the last few days of the month, global currency and bond markets saw a dramatic increase in volatility, as the government of the United Kingdom announced a spending package designed to stimulate the economy. But that would also likely add to inflation pressures and the announcement resulted in a spike in global bond yields while the pound collapsed to an all-time low vs. the dollar, adding to general macroeconomic volatility.

The combination of sticky inflation, expectations of numerous future Fed rate hikes, rising geopolitical tensions, and currency and bond market volatility weighed heavily on stocks and bonds into the end of September, as both markets finished the quarter near the lows for the year.

In sum, the third quarter started with optimism surrounding a resilient corporate earnings outlook, a potential peak in inflation, and a closer-than-expected end to the current Fed rate hiking cycle. But throughout August and September that optimism was eroded by sticky inflation data and a more hawkish-than-expected Federal Reserve.

As we start the fourth quarter markets remain in search of concrete positive catalysts that signal declining inflation pressures and a less-aggressive Federal Reserve.

Third Quarter Performance Review

All four major stock indices posted negative returns for the third consecutive quarter, although unlike the first two quarters of 2022, the tech-heavy Nasdaq did not badly lag other indices and the quarterly declines were fairly uniform across the most widely followed U.S. equity indexes.

By market capitalization, small-cap stocks outperformed large-cap stocks for the first time this year, although the performance gap was modest. Small-cap outperformance came mostly from gains early in the third quarter as markets broadly rallied on hopes of a quick decline in inflation and a sooner-than-expected Fed pivot. But as those hopes faded in late August and September and interest rates hit new highs, investors rotated back to the perceived safety of large-cap stocks, diminishing the performance gap between small and large-caps significantly.

From an investment style standpoint, both value and growth registered losses for the second straight quarter. However, unlike the first half of 2022, growth relatively outperformed value in the third quarter. Growth enjoyed a strong rebound early in the quarter, again as markets rallied on the hope of peak inflation and a Fed pivot that would signal a peak in interest rates. However, that growth outperformance shrank late in the quarter as inflation remained high and the Fed signaled there was no imminent end to the rate hiking cycle.

On a sector level, just one of the 11 S&P 500 sectors finished the third quarter with a positive return. Consumer discretionary posted a positive return thanks to strong consumer spending and still-low unemployment. The energy sector, meanwhile, finished the quarter with a fractional loss as energy stocks benefitted from solid earnings and strength in natural gas prices. More broadly, traditionally defensive sectors relatively outperformed over the past three months, as investors positioned for slower future economic growth.

Sector laggards in the quarter included communication services, real estate, and materials. Communication services have lagged throughout 2022 as investors shunned expensively valued tech companies. Real estate, meanwhile, declined in the face of spiking mortgage rates and as home price appreciation began to slow.

Finally, the materials sector traded lower following earnings warnings from multiple chemical companies and a sharp drop in certain commodities prices in the third quarter, which was driven by a stronger dollar and growing worries about the global economy.

Internationally, foreign markets badly underperformed U.S. markets during the third quarter, as surging electricity prices in Europe and the U.K., interest rate hikes by the European Central Bank and Bank of England, and lasting geopolitical risks weighed heavily on foreign developed markets. Emerging markets, meanwhile, underperformed both foreign developed markets and U.S. markets as a surging U.S. dollar offset hopes for a continued economic reopening in China.

Commodities dropped sharply in the third quarter as a combination of a multi-decade high in the U.S. dollar, growing fears of a global recession, and sharply rising real interest rates weighed on industrial commodities as well as traditional safe havens like precious metals. Oil prices fell in the quarter as concerns about future demand offset geopolitically based worries about supply. Gold, meanwhile, logged solidly negative returns for the second straight quarter thanks to rapidly rising real yields, the surging dollar, and fading market-based inflation expectations.

Switching to fixed-income markets, most bond indices posted solidly negative returns for the third straight quarter. Stubbornly elevated inflation, continued Fed rate hikes, and a late-quarter selloff in global sovereign bonds (driven by the ill-conceived fiscal spending package from the United Kingdom) saw most bond classes end the third quarter lower, extending the year-to-date declines.

Looking deeper into the bond markets, as has been the case all year, shorter-term Treasury Bills outperformed longer-duration Treasury Notes and Bonds as the threat of greater than previously expected Fed rate hikes and still-high inflation weighed on fixed income products with longer durations. For the second straight quarter, short-term Treasury Bills finished the quarter with a slightly positive return.

Corporate bonds relatively outperformed longer-duration government bonds in the third quarter thanks mostly to still-solid U.S. economic data. Higher yielding, lower quality corporate debt declined less than investment grade corporate bonds as resilient corporate earnings kept default risks generally low.

Fourth Quarter Market Outlook

As we start the final quarter of 2022, an honest assessment of the macroeconomic landscape reveals that the markets and the economy are still facing numerous challenges from still-high inflation, ongoing Fed rate hikes, and geopolitical instability.

But while the outlook for risk assets remains challenged, that reality must be considered in the context of a market that has declined substantially and, presumably, already priced in a lot of “bad news.” Valuations on many quality companies are quickly approaching pre-pandemic levels, while the S&P 500 more broadly is trading at a valuation that has, historically speaking, been attractive over the longer term.

Additionally, multiple sentiment indicators have hit or are approaching levels that historically have represented extreme pessimism and bearishness, and they are largely ignoring the reality that there has been some improvement in the macroeconomic outlook over the past several months.

First, inflation has likely peaked. Multiple inflation indicators are showing a peak and decline in price pressures, and while the Consumer Price Index remains far above the Fed’s target of 2%, any swift deceleration in inflation would likely be a material positive catalyst for both stocks and bonds.

Second, the less-aggressive Fed pivot will still occur, perhaps as early as the fourth quarter. According to the Fed’s estimates, interest rate increases will begin to slow in the coming months, and the last rate hike for this cycle could occur in March 2023 or sooner. If that turns out to be the case, and the Fed signals to markets that this rate hike cycle is approaching its end, that will likely be a materially positive catalyst for both stocks and bonds, and that’s evidenced by the July and August rallies that were driven by hopes of a less-aggressive Fed.

Third, geopolitical tensions remain very elevated as Russia has recently escalated the war in Ukraine and the risk of a broader conflict simply can’t be ruled out. But most Western countries remain united in their opposition to the Russian invasion of Ukraine and that will continue to be a powerful deterrent to Russian President Putin.

Additionally, even some of Russia’s most important allies, including China and India, have voiced concerns about the escalation of the war over the past month which has further isolated Russia from the global community. Any reduction in geopolitical tensions would provide a surprise boost for global risk assets, including U.S. stocks and bonds.

Finally, amidst a difficult macroeconomic backdrop, the U.S. economy and corporate America have proven impressively resilient. Most measures of U.S. economic growth remain in solid shape, while U.S. corporate earnings estimates have stayed largely elevated, and the widespread earnings declines that were feared back in early 2022 simply have not materialized.

Bottom line, the outlook for markets and the economy remains challenged, but investors have again priced in a lot of “bad” news already, with valuations now at levels that are historically attractive.

Additionally, according to some indicators, sentiment is as pessimistic as it was during the depths of the financial crisis, and if inflation suddenly decelerates quickly, the Fed signals a clear end to rate hikes, or there’s positive geopolitical news, the potential is there for a powerful rally in both stocks and bonds.

This is a difficult market and a complicated moment for the world, but history is clear: Positive surprises can and have occurred even in difficult times such as this, and through periods of similar macroeconomic turmoil, markets eventually recouped the losses and moved to meaningful new highs. There is no reason to think this time will be any different.

We understand the risks facing both the markets and the economy, and we are committed to helping you effectively navigate this challenging investment environment. Successful investing is a marathon, not a sprint, and even extended bouts of volatility like we’ve experienced so far this year are unlikely to alter a diversified approach set up to meet your long-term investment goals.

As always, we will remain patient and stick to the long-term plan, as we’ve worked with you to establish a unique, personal allocation target based on your financial position, risk tolerance, and investment timeline.

Rest assured that our entire team will remain dedicated to helping you successfully navigate this market environment.

Please do not hesitate to contact us with any questions, comments, or to schedule a portfolio/financial plan review.

Sincerely,

Mike Minter, CFP®, CFS®

Senior Portfolio Manager

Recent Posts

Your “Magic” Retirement Number?

The Market Pullback, Geopolitical Risks, Inflation, and More

Week in Perspective: Stocks Startled by Inflation, Conflict [Apr. 15-2024] – VIDEO

Subscribe to Our Blog

Shareholder | Chief Investment Officer