The challenge facing investors today isn’t whether artificial intelligence will transform the economy, but how to maintain portfolio balance as the market climbs to new all-time highs. While it’s tempting to focus exclusively on companies that have performed well recently, investing for long-term goals requires a thoughtful approach to both growth and risk management.

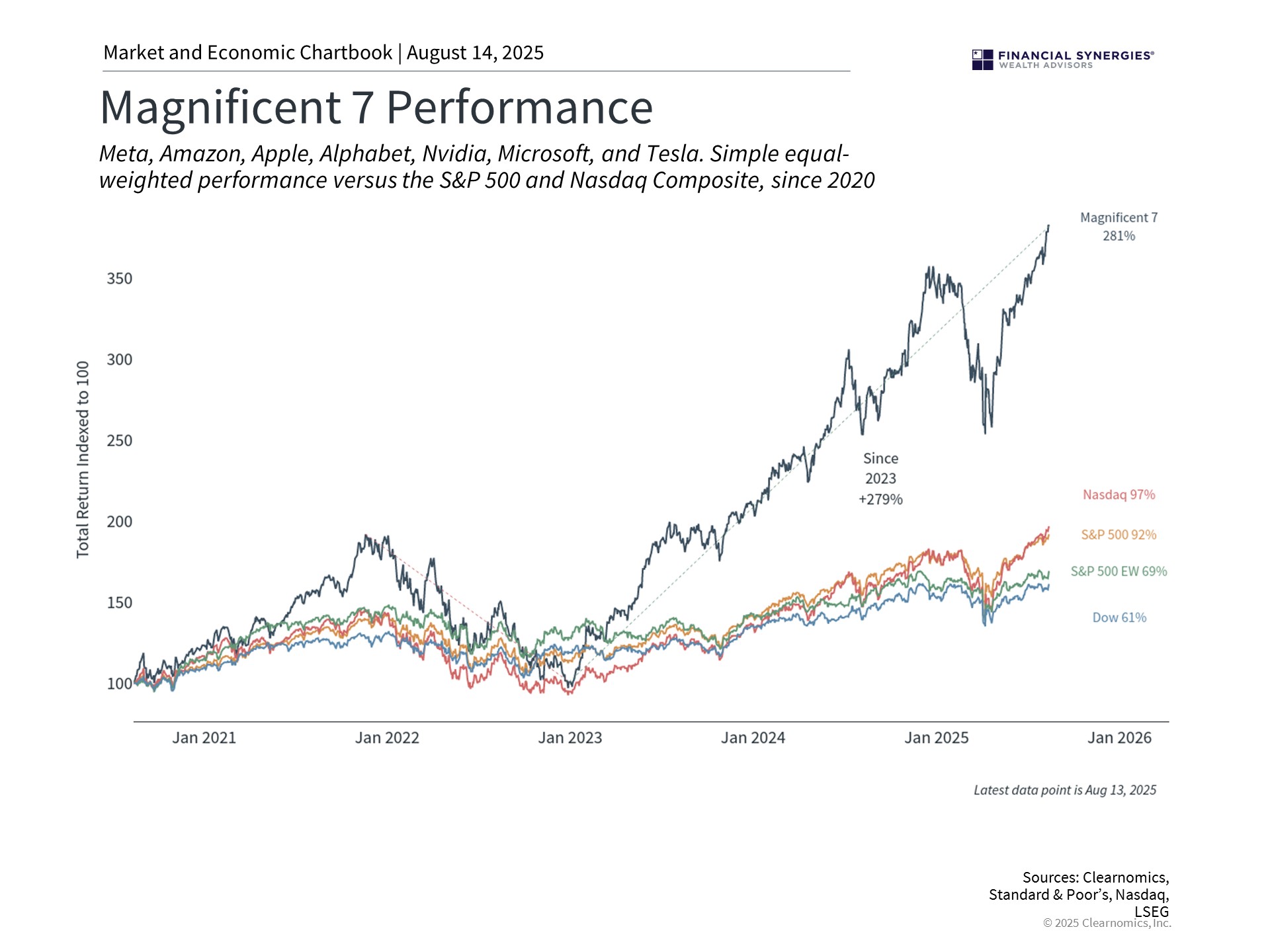

Mega-cap technology stocks, including those benefiting from AI trends, are commonly represented by a group known as the “Magnificent 7.” These stocks – Apple, Microsoft, Nvidia, Amazon, Alphabet, Meta, and Tesla – now constitute about 35% of the S&P 500 and represent seven of the eight largest companies. Several are also referred to as “hyperscalers” due to their significant investments in computing infrastructure to meet the growing demands of AI applications.

In market environments like these, when a relatively small group of stocks drives much of the market’s performance, it becomes even more important to focus on historical perspectives, current valuations, and asset allocation.

Understanding how similar periods of market concentration have played out in the past can help investors make better decisions about their long-term financial plans.

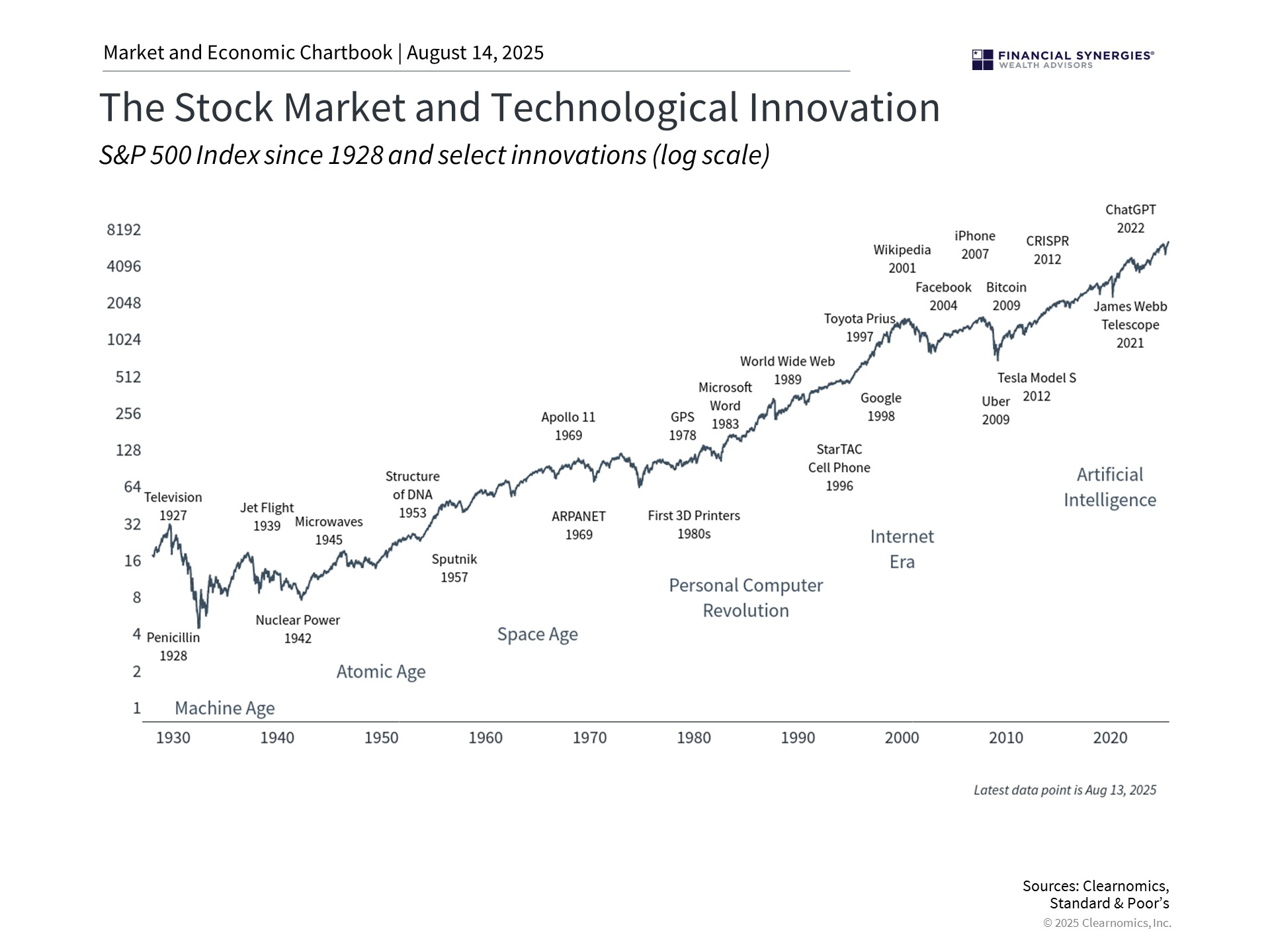

Innovation drives markets in the long run

It may seem as if AI and railroads have little in common, but these transformative technologies often follow similar patterns. In the 1860s, railroad stocks dominated American markets much like technology stocks do today. In fact, the Pennsylvania Railroad company was once the largest company in the world and, alongside other railroads, represented a significant share of the overall stock market. Naturally, this created market enthusiasm and rising valuations that would sound familiar to modern investors.

This pattern has repeated many times across history. The dot-com boom of the 1990s, during which investors focused almost exclusively on internet companies, provides perhaps the clearest recent example. But going as far back as the 19th century, the telegraph, electric power, and telephones transformed cities and created many new companies. In the 20th century, the electronics and computer revolution reshaped all aspects of life and business, even before the invention of the internet.

Each of these waves followed a similar pattern: skepticism, rapid adoption, market enthusiasm, and eventual integration into the broader economy. Railroads didn’t disappear but became a standard part of the transportation and shipping industry, supporting the overall economy. While many dot-com companies did fail in the late 1990s and early 2000s, many others went on to become today’s technology leaders.

When it comes to long-term investing, it’s important to focus not just on individual companies, but on the impact of new technologies on the broader market and economy. After all, the true impact of innovation is greater productivity and efficiency across all businesses. The key difference is that while the stock prices of individual companies may rise and fall quickly, it takes much longer for the full economy-wide effects to be felt.

Valuations matter as much as growth

Today, the question isn’t whether AI will matter, but whether current valuations are reasonable. With the overall S&P 500 trading at a 22.5x price-to-earnings ratio, one that is approaching the all-time high of 24.5x, investors are paying a price that assumes these trends will continue at the same pace.

What’s driving high valuations for the Magnificent 7? First, according to recent estimates, U.S. private AI investment reached $109 billion in 2024, with hundreds of billions more announced this year. This exceeds the entire GDP of many countries and dwarfs similar investments by others.

In recent quarters, investors have reacted positively to announcements of ever-higher AI infrastructure spending. This is a significant shift from less than a year ago when investors were worried about whether these investments by large companies would pay off.

Second, many companies and everyday users have rapidly adopted AI tools, creating more and more demand for computing power. This explains why “hyperscalers” like Microsoft and NVIDIA have seen their market capitalizations soar, with both companies reaching valuations over $4 trillion. This is also why demand for new data centers, and the power needed to run them, are top of mind for investors.

These companies are seen as building the infrastructure that allows other businesses to adopt AI technologies, much like railroad companies built the transportation infrastructure that supported all businesses in the 19th century. While this creates enormous long-term value, the timeline for realizing returns is difficult to predict.

The challenge is that markets often overestimate the speed at which transformative technologies will generate profits, even when the long-term potential may be real. The 1990s offer a cautionary parallel. During that decade, some investors believed that traditional valuation metrics no longer applied to internet companies. When reality didn’t meet expectations, the Nasdaq fell 78% from its peak, and many companies failed or were acquired. Yet the internet did transform the economy, just not within the timeline or in the manner that peak valuations implied.

Balancing opportunities with concentration risk

Similarly, while the Magnificent 7 companies may have led the market on the way up, they have also done so on the way down. For example, in 2022 when interest rates rose quickly due to inflation, these stocks dropped about 50% on average.

Since the Magnificent 7 now represents such a large portion of major market indices, the reality is that nearly all investors have these stocks in their portfolios. For those who have focused on technology stocks, their portfolio allocations may be greater than intended.

Holding too much of a portfolio in just a few investments is often known as “concentration risk,” and is the opposite of diversification. On the one hand, these companies have demonstrated growth and profitability. On the other hand, having a large portion of your portfolio dependent on a small group of companies, regardless of how successful they are, can create volatility as trends change. Even great companies can experience periods of underperformance.

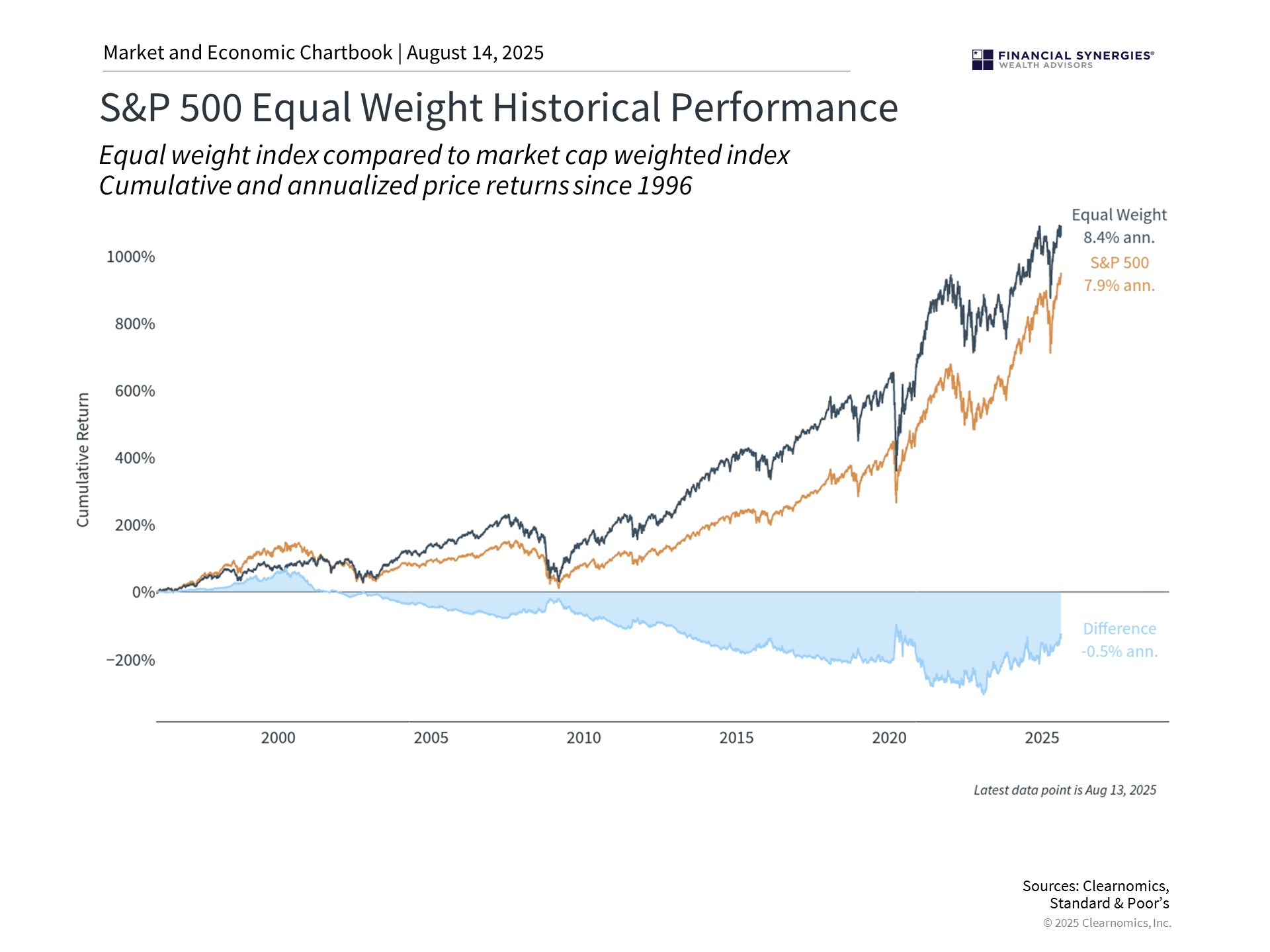

For perspective, consider the equal-weighted S&P 500 shown in the chart above, which gives the same importance to each company regardless of size. This approach has historically provided different return patterns than the standard market-capitalization weighted index, sometimes performing better when large companies struggle.

Since mega cap tech companies have performed well recently, some investors may find it surprising that an equal weighted index has still outperformed over the past 30 years. This highlights the importance of not just focusing on what has driven markets recently and what happens to be in the headlines.

This doesn’t mean that investors should avoid technology stocks (that would be a mistake). Rather, it suggests the importance of maintaining balance and an appropriate asset allocation.

Concerns or questions about how your investment portfolio will hold up in the current market environment? Contact Financial Synergies today.

We are a boutique, financial advisory and total wealth management firm with over 35 years helping clients navigate turbulent markets. To learn more about our approach to investment management please reach out to us. One of our seasoned advisors would be happy to help you build a custom financial plan to help ensure you accomplish your financial goals and objectives. Schedule a conversation with us today.

More relevant articles by Financial Synergies:

Blog Disclosures

This content, which contains security-related opinions and/or information, is provided for informational purposes only and should not be relied upon in any manner as professional advice, or an endorsement of any practices, products or services. There can be no guarantees or assurances that the views expressed here will be applicable for any particular facts or circumstances, and should not be relied upon in any manner. You should consult your own financial advisors as to legal, business, tax, and other related matters concerning any investment.

The commentary in this “post” (including any related blogs, videos, and social media) reflects the personal opinions, viewpoints, and analyses of the Financial Synergies Wealth Advisors, Inc. employees providing such comments, and should not be regarded as the views of Financial Synergies Wealth Advisors, Inc. or its respective affiliates or as a description of advisory services provided by Financial Synergies Wealth Advisors, Inc. or performance returns of any Financial Synergies Wealth Advisors, Inc. client.

Any opinions expressed herein do not constitute or imply endorsement, sponsorship, or recommendation by Financial Synergies Wealth Advisors, Inc. or its employees. The views reflected in the commentary are subject to change at any time without notice.

Nothing on this website constitutes investment or financial planning advice, performance data or any recommendation that any particular security, portfolio of securities, transaction or investment strategy is suitable for any specific person. It also should not be construed as an offer soliciting the purchase or sale of any security mentioned. Nor should it be construed as an offer to provide investment advisory services by Financial Synergies Wealth Advisors, Inc.

Any mention of a particular security and related performance data is not a recommendation to buy or sell that security. Financial Synergies Wealth Advisors, Inc. manages its clients’ accounts using a variety of investment techniques and strategies, which are not necessarily discussed in the commentary. Investments in securities involve the risk of loss. Past performance is no guarantee of future results.

Any charts provided here or on any related Financial Synergies Wealth Advisors, Inc. personnel content outlets are for informational purposes only, and should also not be relied upon when making any investment decision. Any indices referenced for comparison are unmanaged and cannot be invested into directly. As always please remember investing involves risk and possible loss of principal capital; please seek advice from a licensed professional. Any projections, estimates, forecasts, targets, prospects and/or opinions expressed in these materials are subject to change without notice and may differ or be contrary to opinions expressed by others. Information in charts have been obtained from third-party sources and data, and may include those from portfolio securities of funds managed by Financial Synergies Wealth Advisors, Inc. While taken from sources believed to be reliable, Financial Synergies Wealth Advisors, Inc. has not independently verified such information and makes no representations about the enduring accuracy of the information or its appropriateness for a given situation. All content speaks only as of the date indicated.

Financial Synergies Wealth Advisors, Inc. is a registered investment adviser. Advisory services are only offered to clients or prospective clients where Financial Synergies Wealth Advisors, Inc. and its representatives are properly licensed or exempt from licensure. Investments in securities involve the risk of loss. Past performance is no guarantee of future results.

See Full Disclosures Page Here

The Magnificent 7, AI, and Concentration Risk

The challenge facing investors today isn’t whether artificial intelligence will transform the economy, but how to maintain portfolio balance as the market climbs to new all-time highs. While it’s tempting to focus exclusively on companies that have performed well recently, investing for long-term goals requires a thoughtful approach to both growth and risk management.

Mega-cap technology stocks, including those benefiting from AI trends, are commonly represented by a group known as the “Magnificent 7.” These stocks – Apple, Microsoft, Nvidia, Amazon, Alphabet, Meta, and Tesla – now constitute about 35% of the S&P 500 and represent seven of the eight largest companies. Several are also referred to as “hyperscalers” due to their significant investments in computing infrastructure to meet the growing demands of AI applications.

In market environments like these, when a relatively small group of stocks drives much of the market’s performance, it becomes even more important to focus on historical perspectives, current valuations, and asset allocation.

Understanding how similar periods of market concentration have played out in the past can help investors make better decisions about their long-term financial plans.

Innovation drives markets in the long run

It may seem as if AI and railroads have little in common, but these transformative technologies often follow similar patterns. In the 1860s, railroad stocks dominated American markets much like technology stocks do today. In fact, the Pennsylvania Railroad company was once the largest company in the world and, alongside other railroads, represented a significant share of the overall stock market. Naturally, this created market enthusiasm and rising valuations that would sound familiar to modern investors.

This pattern has repeated many times across history. The dot-com boom of the 1990s, during which investors focused almost exclusively on internet companies, provides perhaps the clearest recent example. But going as far back as the 19th century, the telegraph, electric power, and telephones transformed cities and created many new companies. In the 20th century, the electronics and computer revolution reshaped all aspects of life and business, even before the invention of the internet.

Each of these waves followed a similar pattern: skepticism, rapid adoption, market enthusiasm, and eventual integration into the broader economy. Railroads didn’t disappear but became a standard part of the transportation and shipping industry, supporting the overall economy. While many dot-com companies did fail in the late 1990s and early 2000s, many others went on to become today’s technology leaders.

When it comes to long-term investing, it’s important to focus not just on individual companies, but on the impact of new technologies on the broader market and economy. After all, the true impact of innovation is greater productivity and efficiency across all businesses. The key difference is that while the stock prices of individual companies may rise and fall quickly, it takes much longer for the full economy-wide effects to be felt.

Valuations matter as much as growth

Today, the question isn’t whether AI will matter, but whether current valuations are reasonable. With the overall S&P 500 trading at a 22.5x price-to-earnings ratio, one that is approaching the all-time high of 24.5x, investors are paying a price that assumes these trends will continue at the same pace.

What’s driving high valuations for the Magnificent 7? First, according to recent estimates, U.S. private AI investment reached $109 billion in 2024, with hundreds of billions more announced this year. This exceeds the entire GDP of many countries and dwarfs similar investments by others.

In recent quarters, investors have reacted positively to announcements of ever-higher AI infrastructure spending. This is a significant shift from less than a year ago when investors were worried about whether these investments by large companies would pay off.

Second, many companies and everyday users have rapidly adopted AI tools, creating more and more demand for computing power. This explains why “hyperscalers” like Microsoft and NVIDIA have seen their market capitalizations soar, with both companies reaching valuations over $4 trillion. This is also why demand for new data centers, and the power needed to run them, are top of mind for investors.

These companies are seen as building the infrastructure that allows other businesses to adopt AI technologies, much like railroad companies built the transportation infrastructure that supported all businesses in the 19th century. While this creates enormous long-term value, the timeline for realizing returns is difficult to predict.

The challenge is that markets often overestimate the speed at which transformative technologies will generate profits, even when the long-term potential may be real. The 1990s offer a cautionary parallel. During that decade, some investors believed that traditional valuation metrics no longer applied to internet companies. When reality didn’t meet expectations, the Nasdaq fell 78% from its peak, and many companies failed or were acquired. Yet the internet did transform the economy, just not within the timeline or in the manner that peak valuations implied.

Balancing opportunities with concentration risk

Similarly, while the Magnificent 7 companies may have led the market on the way up, they have also done so on the way down. For example, in 2022 when interest rates rose quickly due to inflation, these stocks dropped about 50% on average.

Since the Magnificent 7 now represents such a large portion of major market indices, the reality is that nearly all investors have these stocks in their portfolios. For those who have focused on technology stocks, their portfolio allocations may be greater than intended.

Holding too much of a portfolio in just a few investments is often known as “concentration risk,” and is the opposite of diversification. On the one hand, these companies have demonstrated growth and profitability. On the other hand, having a large portion of your portfolio dependent on a small group of companies, regardless of how successful they are, can create volatility as trends change. Even great companies can experience periods of underperformance.

For perspective, consider the equal-weighted S&P 500 shown in the chart above, which gives the same importance to each company regardless of size. This approach has historically provided different return patterns than the standard market-capitalization weighted index, sometimes performing better when large companies struggle.

Since mega cap tech companies have performed well recently, some investors may find it surprising that an equal weighted index has still outperformed over the past 30 years. This highlights the importance of not just focusing on what has driven markets recently and what happens to be in the headlines.

This doesn’t mean that investors should avoid technology stocks (that would be a mistake). Rather, it suggests the importance of maintaining balance and an appropriate asset allocation.

Concerns or questions about how your investment portfolio will hold up in the current market environment? Contact Financial Synergies today.

We are a boutique, financial advisory and total wealth management firm with over 35 years helping clients navigate turbulent markets. To learn more about our approach to investment management please reach out to us. One of our seasoned advisors would be happy to help you build a custom financial plan to help ensure you accomplish your financial goals and objectives. Schedule a conversation with us today.

More relevant articles by Financial Synergies:

Blog Disclosures

This content, which contains security-related opinions and/or information, is provided for informational purposes only and should not be relied upon in any manner as professional advice, or an endorsement of any practices, products or services. There can be no guarantees or assurances that the views expressed here will be applicable for any particular facts or circumstances, and should not be relied upon in any manner. You should consult your own financial advisors as to legal, business, tax, and other related matters concerning any investment.

The commentary in this “post” (including any related blogs, videos, and social media) reflects the personal opinions, viewpoints, and analyses of the Financial Synergies Wealth Advisors, Inc. employees providing such comments, and should not be regarded as the views of Financial Synergies Wealth Advisors, Inc. or its respective affiliates or as a description of advisory services provided by Financial Synergies Wealth Advisors, Inc. or performance returns of any Financial Synergies Wealth Advisors, Inc. client.

Any opinions expressed herein do not constitute or imply endorsement, sponsorship, or recommendation by Financial Synergies Wealth Advisors, Inc. or its employees. The views reflected in the commentary are subject to change at any time without notice.

Nothing on this website constitutes investment or financial planning advice, performance data or any recommendation that any particular security, portfolio of securities, transaction or investment strategy is suitable for any specific person. It also should not be construed as an offer soliciting the purchase or sale of any security mentioned. Nor should it be construed as an offer to provide investment advisory services by Financial Synergies Wealth Advisors, Inc.

Any mention of a particular security and related performance data is not a recommendation to buy or sell that security. Financial Synergies Wealth Advisors, Inc. manages its clients’ accounts using a variety of investment techniques and strategies, which are not necessarily discussed in the commentary. Investments in securities involve the risk of loss. Past performance is no guarantee of future results.

Any charts provided here or on any related Financial Synergies Wealth Advisors, Inc. personnel content outlets are for informational purposes only, and should also not be relied upon when making any investment decision. Any indices referenced for comparison are unmanaged and cannot be invested into directly. As always please remember investing involves risk and possible loss of principal capital; please seek advice from a licensed professional. Any projections, estimates, forecasts, targets, prospects and/or opinions expressed in these materials are subject to change without notice and may differ or be contrary to opinions expressed by others. Information in charts have been obtained from third-party sources and data, and may include those from portfolio securities of funds managed by Financial Synergies Wealth Advisors, Inc. While taken from sources believed to be reliable, Financial Synergies Wealth Advisors, Inc. has not independently verified such information and makes no representations about the enduring accuracy of the information or its appropriateness for a given situation. All content speaks only as of the date indicated.

Financial Synergies Wealth Advisors, Inc. is a registered investment adviser. Advisory services are only offered to clients or prospective clients where Financial Synergies Wealth Advisors, Inc. and its representatives are properly licensed or exempt from licensure. Investments in securities involve the risk of loss. Past performance is no guarantee of future results.

See Full Disclosures Page Here

Recent Posts

The Magnificent 7, AI, and Concentration Risk

How Reliable is Government Data? A Balanced Look

Last Week on Wall Street: Stocks Rise on Earnings, Despite Tariffs [Aug. 11-2025]

Subscribe to Our Blog

Shareholder | Chief Investment Officer