The corporate earnings season kicks off this week amid concerns of slowing economic growth. It’s understandable that some investors are worried about how this could affect corporate earnings and their investment returns. What is the earnings outlook for 2019 and how should investors maintain perspective in this market environment?

Corporate earnings growth is a fundamental component of stock returns. We can think of stock returns as growth in earnings coupled with a change in valuations. In other words, stock prices go up if corporations are more profitable, if investors are willing to pay more for that profitability, or both. Thus, the fact that the economy expands and companies become more profitable is a key reason that stock prices rise over the long run.

The past ten years have been no exception. The earnings-per-share of S&P 500 companies has grown by 170% since the bottom in 2009, and 72% since the last cycle peak in 2007. Of all of the reasons that stocks have risen 280% over that period, earnings growth is the most important.

Last year saw a continuation of this trend with earnings growing nearly 24%, from $129 per share to an estimated $159. This is a spectacular pace of growth that will decelerate. Over the past 30 years, the average growth rate has been far lower at roughly 7%.

It’s also important to remember that there was an “earnings recession” just a few years ago. Beginning in 2014, oil prices collapsed and the U.S. dollar spiked, which caused U.S. earnings to shrink for several quarters. This ended in 2017 when these factors stabilized and global growth surged.

At the moment, earnings are expected to grow by 7% in 2019, roughly the same as the historical average. Whether there will be surprises to the upside or downside will depend on trends in global growth, economic policy, and profit margins.

Thus, there are three important things to understand about earnings growth. First, earnings growth may decelerate, but this is from an unsustainable breakneck pace in 2018. Second, even if growth is slower, earnings could still continue to grow at a solid pace. This should be far different from the earnings recession of a few years ago when earnings actually shrank.

Finally, even an earnings growth rate in the neighborhood of 7% is enough to support strong stock market returns for investors. Of course, it’s impossible to predict returns over any given quarter or year. Additionally, there may be more volatility and uncertainty since we’re later in the economic cycle.

1. Corporate earnings should continue to grow, but at a slower pace.

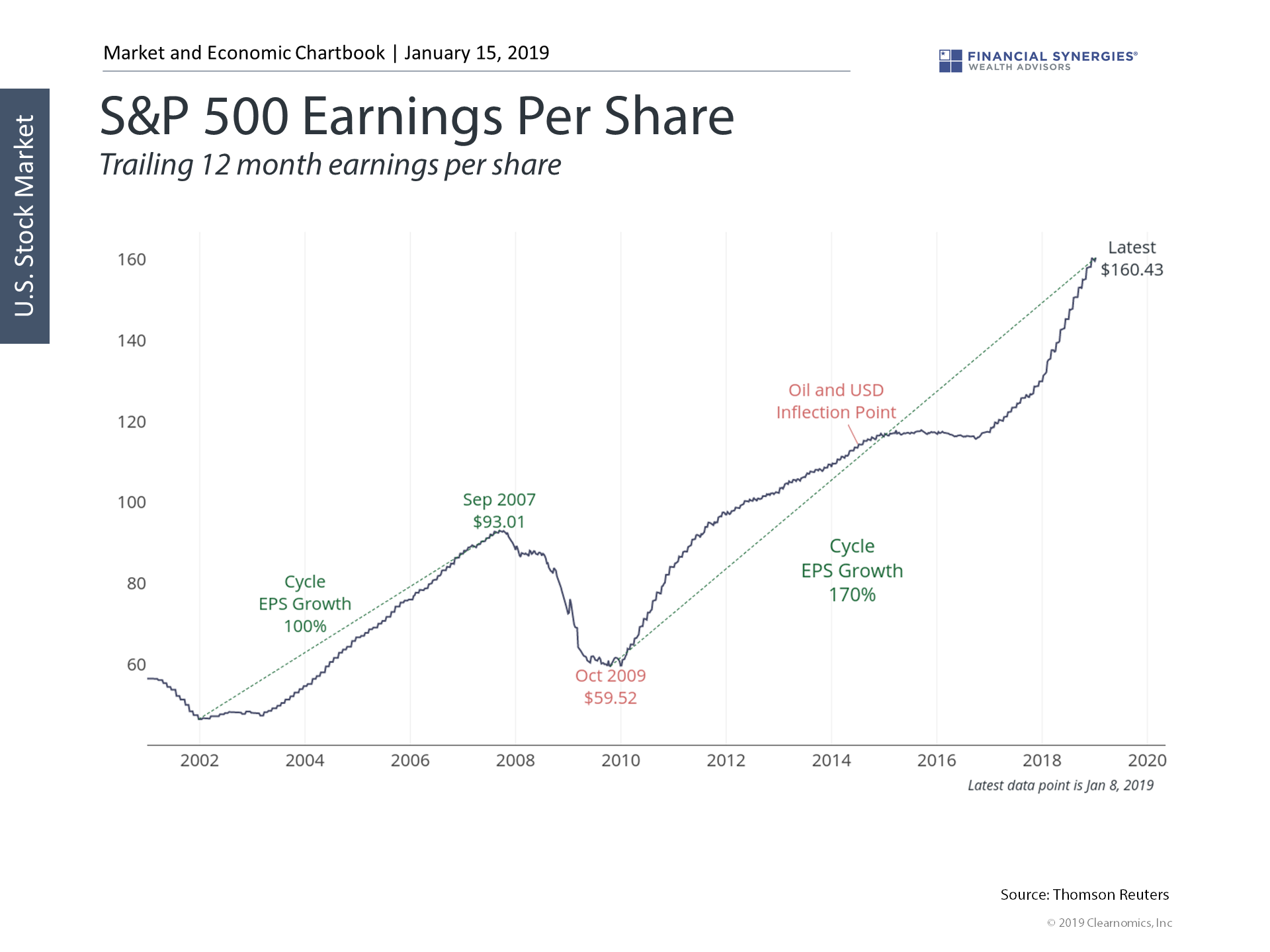

S&P 500 Earnings Per Share

Corporate profits have been a dominant driver of markets over the past ten years. Earnings have risen 170% since the recession, propelling stocks to new highs over this period. After spectacular earnings in 2018, it’s only natural that the rate of growth will decelerate – not that earnings will actually fall.

Corporate profits have been a dominant driver of markets over the past ten years. Earnings have risen 170% since the recession, propelling stocks to new highs over this period. After spectacular earnings in 2018, it’s only natural that the rate of growth will decelerate – not that earnings will actually fall.

Earnings growth flat-lined from 2014 – 2016 due to collapsing oil prices and a spike in the U.S. dollar, as seen in the chart above. The concerns that many investors have are quite different from what was experienced during that period. Today, earnings are still expected to grow at a healthy pace.

2. Earnings are expected to be healthy across sectors.

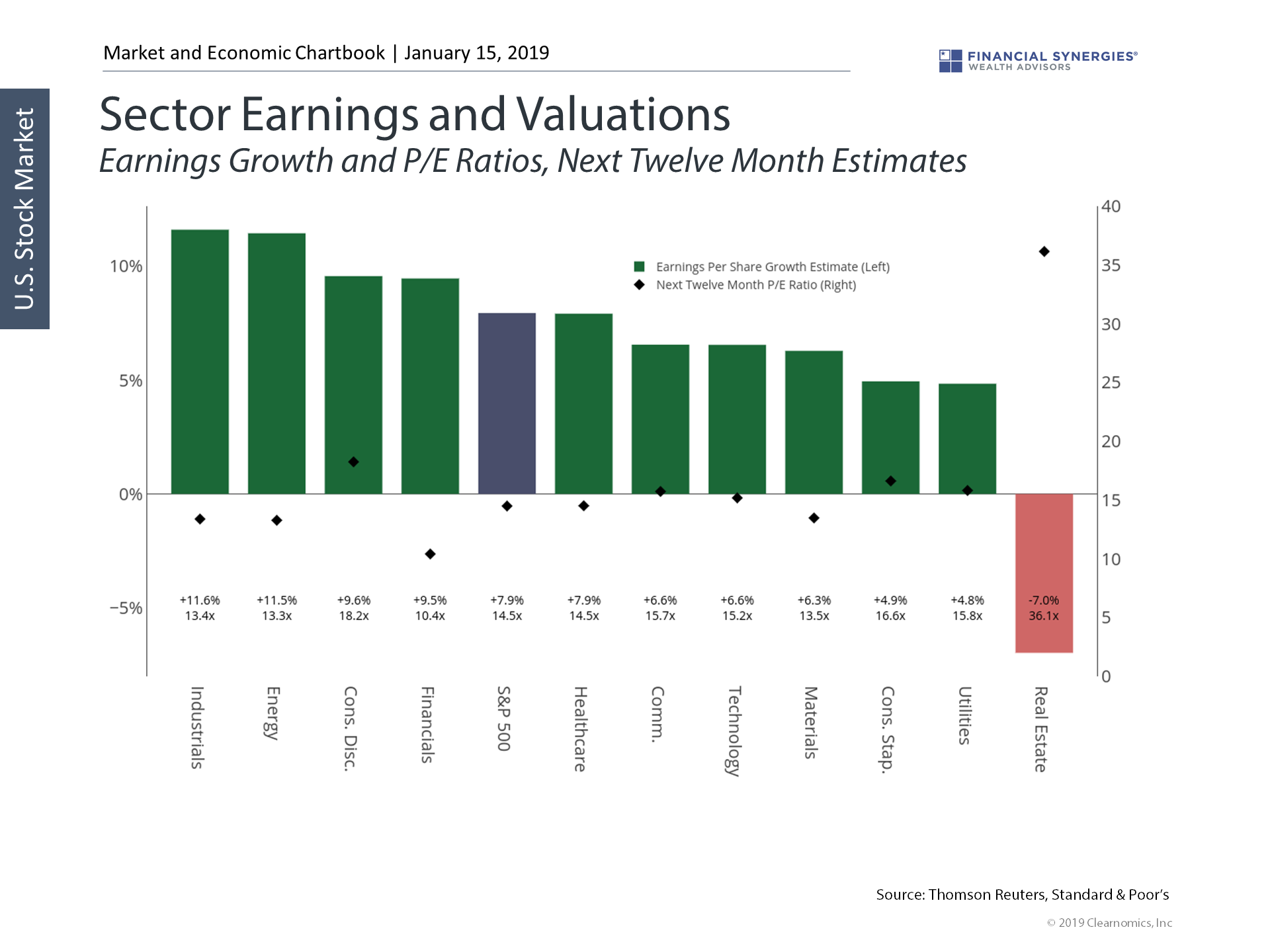

Sector Earnings and Valuations

Most sectors are expecting healthy earnings growth over the next twelve months as well. In fact, 10 of the 11 sectors are expecting positive growth, ranging from nearly 5% to almost 12%. Some of the fastest growing sectors have below-average valuations as well.

The one exception is the real estate sector due to higher interest rates, a slowdown in real estate activity, and other sector-specific factors. Still, this sector has been a source of stability and yield in a volatile market.

3. Global earnings should continue to grow as well.

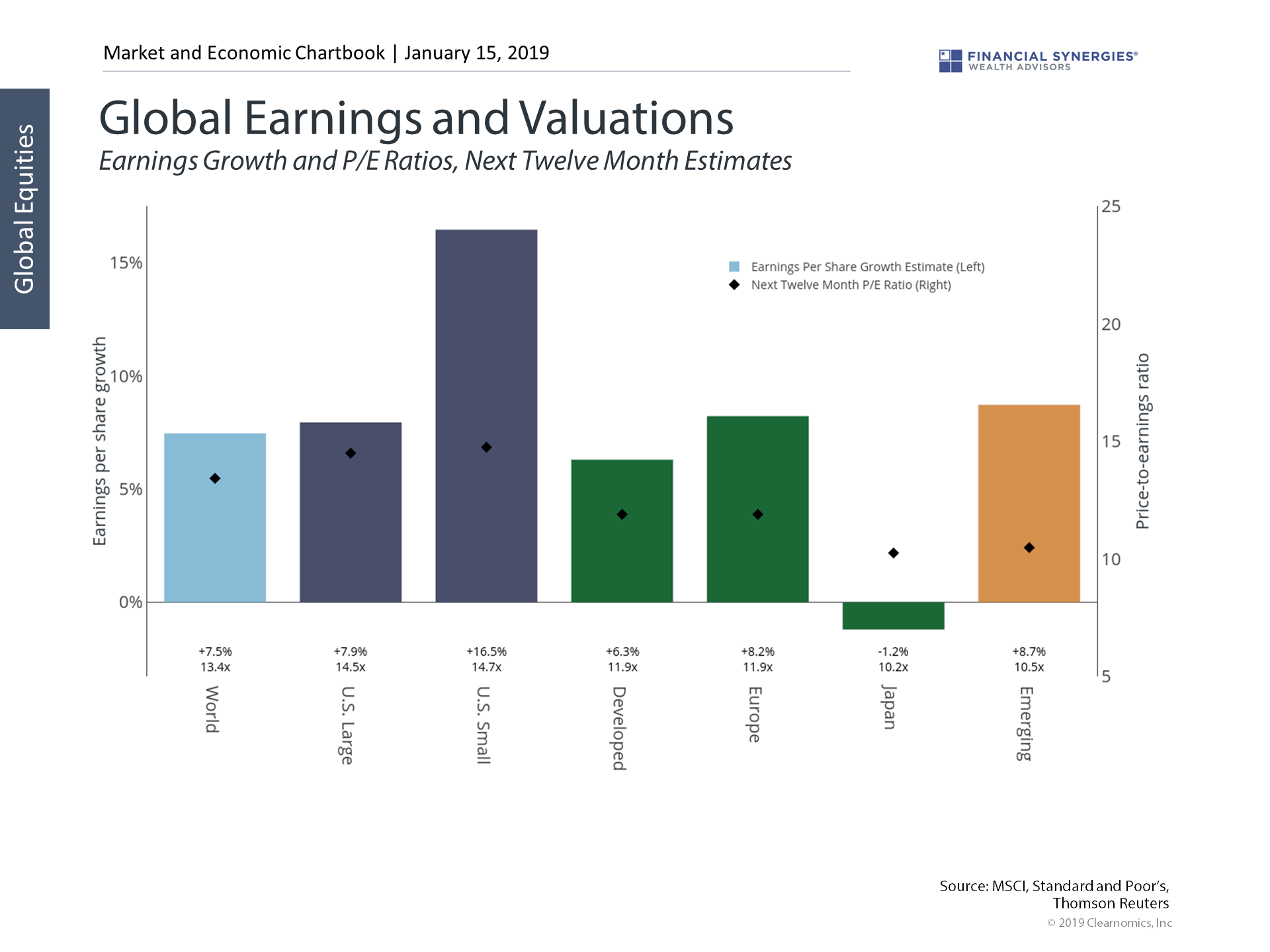

Global Earnings and Valuations

The discussion above focused on U.S. large cap companies. While these companies should continue to see healthy earnings, there are many other parts of the global market that continue to experience growth.

For instance, U.S. small cap stocks are expected to see double the earnings growth rate, at roughly the same level of valuations. Emerging markets and European stocks are also expected to grow earnings more quickly than U.S. large caps, at significantly cheaper valuations.

The bottom line? Earnings growth is at least expected to be healthy. And, as always, it’s important to stay diversified across sectors and global markets.

Source: Clearnomics

Should We Worry About Corporate Earnings In 2019?

The corporate earnings season kicks off this week amid concerns of slowing economic growth. It’s understandable that some investors are worried about how this could affect corporate earnings and their investment returns. What is the earnings outlook for 2019 and how should investors maintain perspective in this market environment?

Corporate earnings growth is a fundamental component of stock returns. We can think of stock returns as growth in earnings coupled with a change in valuations. In other words, stock prices go up if corporations are more profitable, if investors are willing to pay more for that profitability, or both. Thus, the fact that the economy expands and companies become more profitable is a key reason that stock prices rise over the long run.

The past ten years have been no exception. The earnings-per-share of S&P 500 companies has grown by 170% since the bottom in 2009, and 72% since the last cycle peak in 2007. Of all of the reasons that stocks have risen 280% over that period, earnings growth is the most important.

Last year saw a continuation of this trend with earnings growing nearly 24%, from $129 per share to an estimated $159. This is a spectacular pace of growth that will decelerate. Over the past 30 years, the average growth rate has been far lower at roughly 7%.

It’s also important to remember that there was an “earnings recession” just a few years ago. Beginning in 2014, oil prices collapsed and the U.S. dollar spiked, which caused U.S. earnings to shrink for several quarters. This ended in 2017 when these factors stabilized and global growth surged.

At the moment, earnings are expected to grow by 7% in 2019, roughly the same as the historical average. Whether there will be surprises to the upside or downside will depend on trends in global growth, economic policy, and profit margins.

Finally, even an earnings growth rate in the neighborhood of 7% is enough to support strong stock market returns for investors. Of course, it’s impossible to predict returns over any given quarter or year. Additionally, there may be more volatility and uncertainty since we’re later in the economic cycle.

1. Corporate earnings should continue to grow, but at a slower pace.

S&P 500 Earnings Per Share

Earnings growth flat-lined from 2014 – 2016 due to collapsing oil prices and a spike in the U.S. dollar, as seen in the chart above. The concerns that many investors have are quite different from what was experienced during that period. Today, earnings are still expected to grow at a healthy pace.

2. Earnings are expected to be healthy across sectors.

Sector Earnings and Valuations

Most sectors are expecting healthy earnings growth over the next twelve months as well. In fact, 10 of the 11 sectors are expecting positive growth, ranging from nearly 5% to almost 12%. Some of the fastest growing sectors have below-average valuations as well.

The one exception is the real estate sector due to higher interest rates, a slowdown in real estate activity, and other sector-specific factors. Still, this sector has been a source of stability and yield in a volatile market.

3. Global earnings should continue to grow as well.

Global Earnings and Valuations

The discussion above focused on U.S. large cap companies. While these companies should continue to see healthy earnings, there are many other parts of the global market that continue to experience growth.

For instance, U.S. small cap stocks are expected to see double the earnings growth rate, at roughly the same level of valuations. Emerging markets and European stocks are also expected to grow earnings more quickly than U.S. large caps, at significantly cheaper valuations.

The bottom line? Earnings growth is at least expected to be healthy. And, as always, it’s important to stay diversified across sectors and global markets.

Source: Clearnomics

Recent Posts

2nd Quarter 2025 Market and Economic Review

The Market Reaches All-Time Highs

Last Week on Wall Street: Broad-Based Market Rally [June 30-2025]

Subscribe to Our Blog

Shareholder | Chief Investment Officer