The stock market’s strong performance since March has obviously not been shared by all parts of the market. Some sectors, notably technology-driven ones, have fared way better than those directly impacted by the pandemic and social distancing. What’s more, the outsized contribution of tech stocks resulted in a brief period of volatility in September. It’s understandable that this may feel “fragile”, “unsustainable”, or even “artificial” to some investors. How should we respond to these recent dynamics and the changing nature of the stock market?

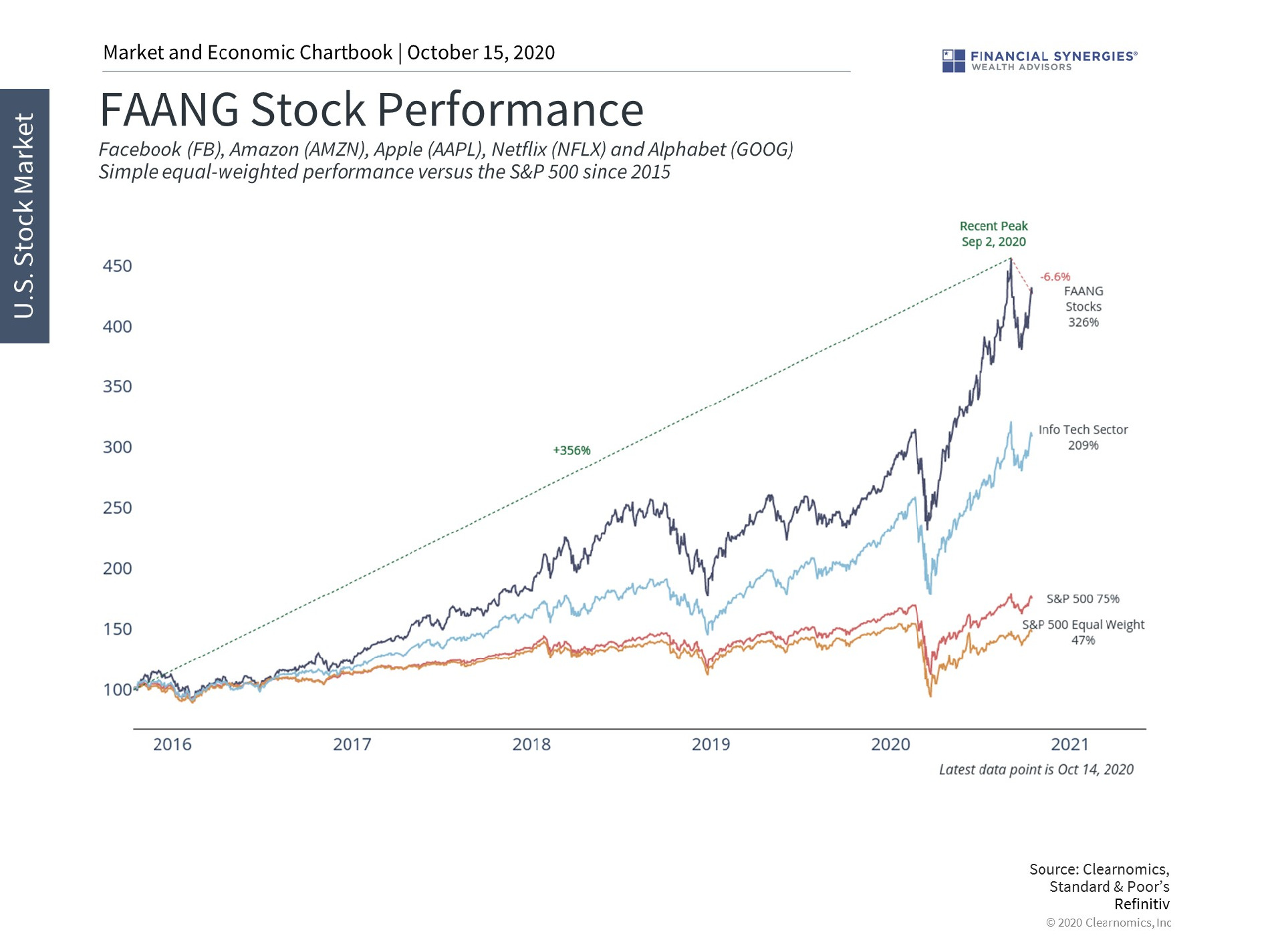

There appear to be two separate but related issues that worry some investors. First, many are concerned by the outperformance of technology-driven stocks. The so-called FAANG stocks, along with other large tech companies and more recent IPOs, have significantly outperformed the rest of the stock market both this year and over the past decade.

Many of these companies have benefited from trends in digital transformation which have only accelerated during the COVID-19 pandemic. In many ways, the performance of these stocks reflects the economic success of the underlying companies. Unlike the dot com bubble of the late 1990s and early 2000s, many of these companies have profitable and proven business models. Although their valuation levels can certainly be debated, the performance of these stocks reflects the fast-changing nature of businesses and the economy.

As a result, it’s also undeniable that the composition of major market indices has shifted over the past decade. The five largest stocks in the S&P 500 are Apple, Amazon, Microsoft, Alphabet (Google), and Facebook. Many sectors are driven by technology stocks including Information Technology, Communication Services and Consumer Discretionary. This trend has also influenced other market factors such as Growth stocks dramatically outperforming Value ones.

The stock market is reflecting the importance of technology companies and the evolution of what is considered a tech stock. For instance, the pandemic and shifting consumer habits have blurred the line between technology and retail. This is not to say that these stocks will outperform forever, and it’s always the case that past performance is no guarantee of the future. However, the rise in these stocks is a reflection of how the economy looks today – a fact that benefits diversified investors. Investors ought to remain balanced across a variety of sectors and styles that are tied to trends in the underlying economy.

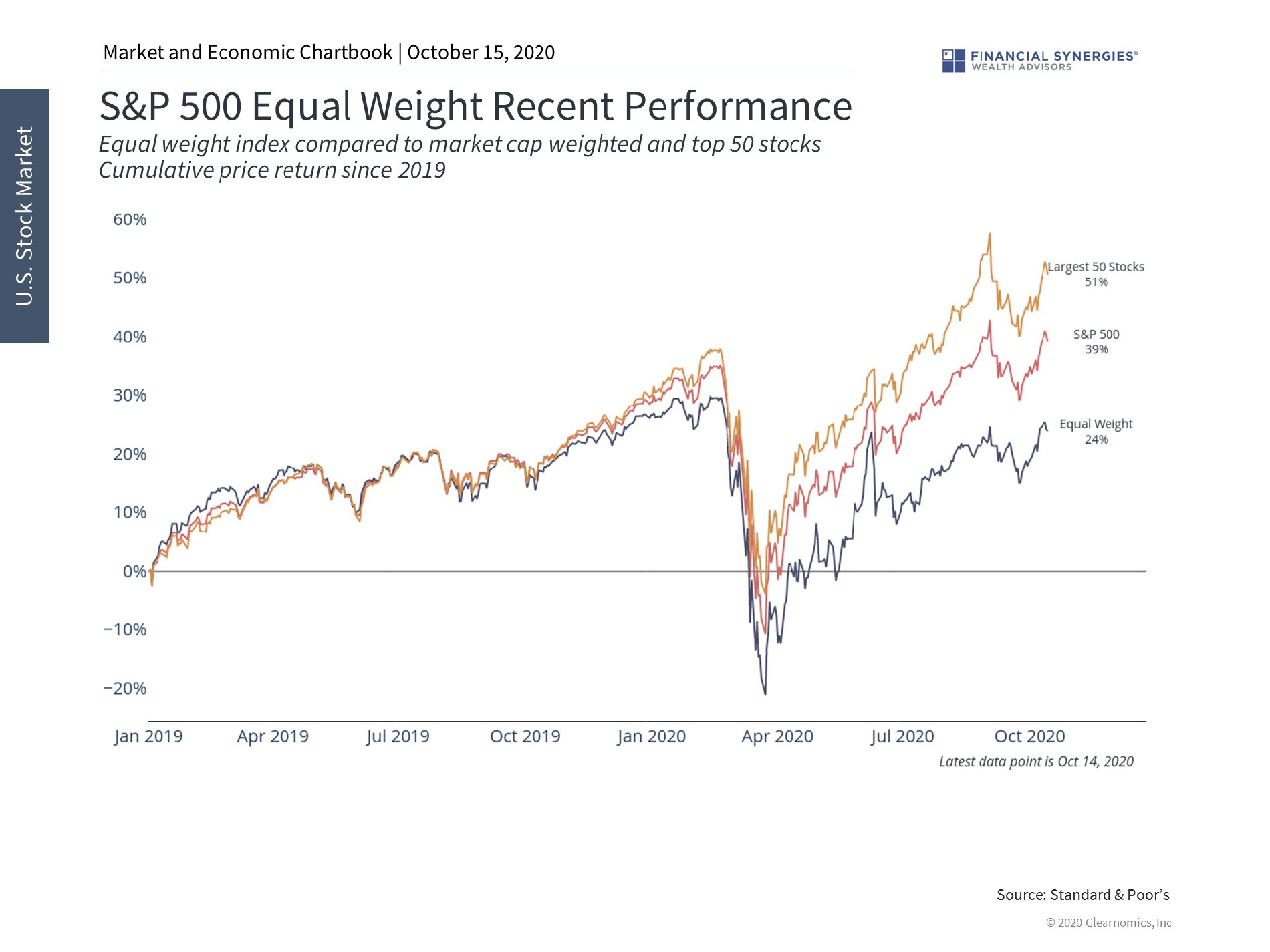

The second issue is that a small group of companies has had an outsized impact on the overall stock market. It’s understandable that this feels untenable for some investors.

Perhaps the simplest way to see this is to compare the standard S&P 500 index, which places a weight on each stock based on its size or market capitalization, to one which gives an equal weight to each stock. The theoretical reasons to use one over the other is beyond the scope of this discussion but suffice it to say there are good reasons for both. Using market cap weights provides a more accurate sense of the composition of the stock market – i.e. where the dollars are. Using equal weights helps investors to benefit from a broader base of companies.

Due to the outperformance of large tech stocks, the market cap-weighted S&P 500 has significantly outperformed its equal weight counterpart. This is even more pronounced when looking at only the largest 50 companies in the S&P 500. Over the past two years, the biggest companies have outperformed the overall index by a cumulative 10%.

But once again, this reflects the growing importance of these large companies to the economy and the world over the past decade. In fact, it’s not the case that large companies necessarily dominate stock market returns. For much of the history of the stock market, the largest companies were often seen as the most boring (e.g. “blue chips”) – perhaps serving as a source of stable dividends, but little more. Over the past 15 years, an equal weight index has actually outperformed the market cap-weighted one since it benefits from returns across a wider array of stocks.

Thus, although mega cap companies have driven overall stock market returns recently, whether this will continue depends on the balance between tech trends and the importance of size/scale to companies.

1. Technology stocks have driven index returns recently

Technology stocks – both mega cap ones and recent IPOs – have helped to propel overall stock market returns this year and over the past decade. The so-called FAANG stocks have outperformed traditional tech-led sectors, which have in turn outperformed the overall stock market. These stocks reflect the fact that their companies have benefited from trends in digital transformation.

2. Overall market returns have been supported by the largest stocks

As a result, the stock market has been influenced by large technology stocks. An equal weight index of S&P 500 stocks has significantly underperformed the market cap-weighted and the top 50 stocks. This trend accelerated in 2020 due to the COVID-19 pandemic.

3. This is not always the case but reflects an evolving market and economy

However, many of these trends are the result of changes to businesses and the economy. Large companies do not always have an out-sized impact on the overall stock market. Historically, an equal weight index has done well too. Thus, investors should continue to stay diversified among all parts of the market to benefit from on-going economic trends.

Source: Clearnomics

How Stock Market Concentration Impacts Investors

The stock market’s strong performance since March has obviously not been shared by all parts of the market. Some sectors, notably technology-driven ones, have fared way better than those directly impacted by the pandemic and social distancing. What’s more, the outsized contribution of tech stocks resulted in a brief period of volatility in September. It’s understandable that this may feel “fragile”, “unsustainable”, or even “artificial” to some investors. How should we respond to these recent dynamics and the changing nature of the stock market?

There appear to be two separate but related issues that worry some investors. First, many are concerned by the outperformance of technology-driven stocks. The so-called FAANG stocks, along with other large tech companies and more recent IPOs, have significantly outperformed the rest of the stock market both this year and over the past decade.

Many of these companies have benefited from trends in digital transformation which have only accelerated during the COVID-19 pandemic. In many ways, the performance of these stocks reflects the economic success of the underlying companies. Unlike the dot com bubble of the late 1990s and early 2000s, many of these companies have profitable and proven business models. Although their valuation levels can certainly be debated, the performance of these stocks reflects the fast-changing nature of businesses and the economy.

As a result, it’s also undeniable that the composition of major market indices has shifted over the past decade. The five largest stocks in the S&P 500 are Apple, Amazon, Microsoft, Alphabet (Google), and Facebook. Many sectors are driven by technology stocks including Information Technology, Communication Services and Consumer Discretionary. This trend has also influenced other market factors such as Growth stocks dramatically outperforming Value ones.

The stock market is reflecting the importance of technology companies and the evolution of what is considered a tech stock. For instance, the pandemic and shifting consumer habits have blurred the line between technology and retail. This is not to say that these stocks will outperform forever, and it’s always the case that past performance is no guarantee of the future. However, the rise in these stocks is a reflection of how the economy looks today – a fact that benefits diversified investors. Investors ought to remain balanced across a variety of sectors and styles that are tied to trends in the underlying economy.

The second issue is that a small group of companies has had an outsized impact on the overall stock market. It’s understandable that this feels untenable for some investors.

Perhaps the simplest way to see this is to compare the standard S&P 500 index, which places a weight on each stock based on its size or market capitalization, to one which gives an equal weight to each stock. The theoretical reasons to use one over the other is beyond the scope of this discussion but suffice it to say there are good reasons for both. Using market cap weights provides a more accurate sense of the composition of the stock market – i.e. where the dollars are. Using equal weights helps investors to benefit from a broader base of companies.

Due to the outperformance of large tech stocks, the market cap-weighted S&P 500 has significantly outperformed its equal weight counterpart. This is even more pronounced when looking at only the largest 50 companies in the S&P 500. Over the past two years, the biggest companies have outperformed the overall index by a cumulative 10%.

But once again, this reflects the growing importance of these large companies to the economy and the world over the past decade. In fact, it’s not the case that large companies necessarily dominate stock market returns. For much of the history of the stock market, the largest companies were often seen as the most boring (e.g. “blue chips”) – perhaps serving as a source of stable dividends, but little more. Over the past 15 years, an equal weight index has actually outperformed the market cap-weighted one since it benefits from returns across a wider array of stocks.

Thus, although mega cap companies have driven overall stock market returns recently, whether this will continue depends on the balance between tech trends and the importance of size/scale to companies.

1. Technology stocks have driven index returns recently

Technology stocks – both mega cap ones and recent IPOs – have helped to propel overall stock market returns this year and over the past decade. The so-called FAANG stocks have outperformed traditional tech-led sectors, which have in turn outperformed the overall stock market. These stocks reflect the fact that their companies have benefited from trends in digital transformation.

2. Overall market returns have been supported by the largest stocks

As a result, the stock market has been influenced by large technology stocks. An equal weight index of S&P 500 stocks has significantly underperformed the market cap-weighted and the top 50 stocks. This trend accelerated in 2020 due to the COVID-19 pandemic.

3. This is not always the case but reflects an evolving market and economy

However, many of these trends are the result of changes to businesses and the economy. Large companies do not always have an out-sized impact on the overall stock market. Historically, an equal weight index has done well too. Thus, investors should continue to stay diversified among all parts of the market to benefit from on-going economic trends.

Source: Clearnomics

Recent Posts

2nd Quarter 2025 Market and Economic Review

The Market Reaches All-Time Highs

Last Week on Wall Street: Broad-Based Market Rally [June 30-2025]

Subscribe to Our Blog

Shareholder | Chief Investment Officer