How Do Withdrawal Rates Impact Your Portfolio in Retirement?

Many people spend years preparing for retirement by saving and investing, but planning shouldn’t stop once the paychecks do.

For your convenience, we’ve also provided a PDF copy of the Chart of the Month | How do Withdrawal Rates Impact Your Portfolio in Retirement?

Transitioning from earning income to withdrawing it from your portfolio is a major shift with a new set of risks and decisions. This period, known as the distribution phase, requires careful thought. How much you withdraw each year can have a bigger impact on long-term financial security than many people realize. Without a well-structured strategy, even a sizable retirement account can be depleted faster than expected.

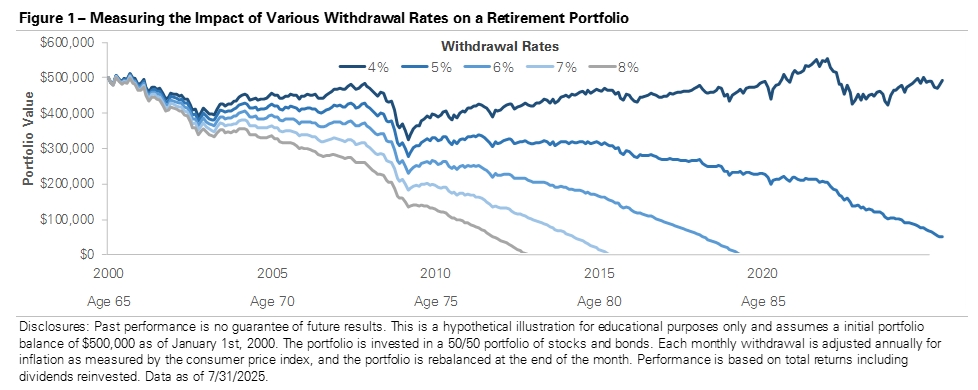

The chart below shows how different withdrawal rates can impact a retirement portfolio’s lifespan. It assumes an individual retired in 2000 at age 65 with $500,000 and started taking monthly withdrawals. Each line reflects a different withdrawal rate between 4% and 8%, showing how the portfolio fared through age 85. While all scenarios start at the same point, the paths quickly diverge, especially during periods of market volatility. The chart illustrates how a retiree’s withdrawal strategy can determine whether the portfolio lasts or runs out.

The message is clear: higher withdrawal rates tend to exhaust a portfolio sooner, while lower rates can extend its life. In this example, withdrawing 7% or 8% caused the portfolio to run out of money before age 85. In contrast, the 4% and 5% withdrawal rates helped the portfolio weather market declines. The 4% strategy not only preserved the portfolio but grew it over 20 years, showing how compounding can work even during retirement.

No strategy can eliminate market risk, but a smaller withdrawal rate can extend the portfolio’s life and reduce the risk of outliving your savings. Taking a more conservative withdrawal approach in the early years of retirement gives your portfolio time to recover from short-term losses and grow with the market.

A thoughtful withdrawal strategy is an important part of retirement planning. It’s not just about how much you’ve accumulated, but how you manage it. There’s no one-size-fits-all approach, and the method you start with doesn’t have to be permanent. Fixed withdrawal rates can provide a good starting point, but many retirees may benefit from more flexible approaches. For example, you could adjust withdrawals based on market conditions, taking smaller distributions in down years and larger ones in strong years.

Another option is the bucket strategy, which divides assets into short-, intermediate-, and long-term segments. By keeping 1-2 years’ worth of expenses in cash or short-term investments, you can avoid selling stocks during major market declines, such as those in 2008 or 2020. This gives long-term investments time to recover and can help create a steadier income stream over time.

Everyone’s retirement looks different. Our goal is to help you create a withdrawal strategy tailored to your unique needs and goals when that time comes.

Disclosure

The information and opinions provided herein are provided as general market commentary only – not financial advice – and are subject to change at any time without notice. This commentary may contain forward-looking statements that are subject to various risks and uncertainties. None of the events or outcomes mentioned here may come to pass, and actual results may differ materially from those expressed or implied in these statements. No mention of a particular security, index, or other instrument in this report constitutes a recommendation to buy, sell, or hold that or any other security, nor does it constitute an opinion on the suitability of any security or index. The report is strictly an informational publication and has been prepared without regard to the particular investments and circumstances of the recipient.

Past performance does not guarantee or indicate future results. Any index performance mentioned is for illustrative purposes only and does not reflect any management fees, transaction costs, or expenses. Indexes are unmanaged, and one cannot invest directly in an index. Index performance does not represent the actual performance that would be achieved by investing in a fund.

See Full Disclosures Page

Concerns or questions about how your investment portfolio will hold up in the current market environment? Contact Financial Synergies today.

We are a boutique, financial advisory and total wealth management firm with over 35 years helping clients navigate turbulent markets. To learn more about our approach to investment management please reach out to us. One of our seasoned advisors would be happy to help you build a custom financial plan to help ensure you accomplish your financial goals and objectives. Schedule a conversation with us today.

More relevant articles by Financial Synergies:

Blog Disclosures

This content, which may contain security-related opinions and/or information, is provided for informational purposes only and should not be relied upon in any manner as professional advice, or an endorsement of any practices, products or services. There can be no guarantees or assurances that the views expressed here will be applicable for any particular facts or circumstances, and should not be relied upon in any manner. You should consult your own financial advisors as to legal, business, tax, and other related matters concerning any investment.

The commentary in this “post” (including any related blogs, videos, and social media) reflects the personal opinions, viewpoints, and analyses of the Financial Synergies Wealth Advisors, Inc. employees providing such comments, and should not be regarded as the views of Financial Synergies Wealth Advisors, Inc. or its respective affiliates or as a description of advisory services provided by Financial Synergies Wealth Advisors, Inc. or performance returns of any Financial Synergies Wealth Advisors, Inc. client.

Any opinions expressed herein do not constitute or imply endorsement, sponsorship, or recommendation by Financial Synergies Wealth Advisors, Inc. or its employees. The views reflected in the commentary are subject to change at any time without notice.

Nothing on this website or Blog constitutes investment or financial planning advice, performance data or any recommendation that any particular security, portfolio of securities, transaction or investment strategy is suitable for any specific person. It also should not be construed as an offer soliciting the purchase or sale of any security mentioned. Nor should it be construed as an offer to provide investment advisory services by Financial Synergies Wealth Advisors, Inc.

Any mention of a particular security and related performance data is not a recommendation to buy or sell that security. Financial Synergies Wealth Advisors, Inc. manages its clients’ accounts using a variety of investment techniques and strategies, which are not necessarily discussed in the commentary. Investments in securities involve the risk of loss. Past performance is no guarantee of future results.

Any charts provided here or on any related Financial Synergies Wealth Advisors, Inc. personnel content outlets are for informational purposes only, and should also not be relied upon when making any investment decision. Any indices referenced for comparison are unmanaged and cannot be invested into directly. As always please remember investing involves risk and possible loss of principal capital; please seek advice from a licensed professional. Any projections, estimates, forecasts, targets, prospects and/or opinions expressed in these materials are subject to change without notice and may differ or be contrary to opinions expressed by others. Information in charts have been obtained from third-party sources and data, and may include those from portfolio securities of funds managed by Financial Synergies Wealth Advisors, Inc. While taken from sources believed to be reliable, Financial Synergies Wealth Advisors, Inc. has not independently verified such information and makes no representations about the enduring accuracy of the information or its appropriateness for a given situation. All content speaks only as of the date indicated.

Financial Synergies Wealth Advisors, Inc. is a registered investment adviser. Advisory services are only offered to clients or prospective clients where Financial Synergies Wealth Advisors, Inc. and its representatives are properly licensed or exempt from licensure. Investments in securities involve the risk of loss. Past performance is no guarantee of future results.

See Full Disclosures Page Here

How Do Withdrawal Rates Impact Your Portfolio in Retirement? | Chart of the Month

How Do Withdrawal Rates Impact Your Portfolio in Retirement?

Many people spend years preparing for retirement by saving and investing, but planning shouldn’t stop once the paychecks do.

For your convenience, we’ve also provided a PDF copy of the Chart of the Month | How do Withdrawal Rates Impact Your Portfolio in Retirement?

Transitioning from earning income to withdrawing it from your portfolio is a major shift with a new set of risks and decisions. This period, known as the distribution phase, requires careful thought. How much you withdraw each year can have a bigger impact on long-term financial security than many people realize. Without a well-structured strategy, even a sizable retirement account can be depleted faster than expected.

The chart below shows how different withdrawal rates can impact a retirement portfolio’s lifespan. It assumes an individual retired in 2000 at age 65 with $500,000 and started taking monthly withdrawals. Each line reflects a different withdrawal rate between 4% and 8%, showing how the portfolio fared through age 85. While all scenarios start at the same point, the paths quickly diverge, especially during periods of market volatility. The chart illustrates how a retiree’s withdrawal strategy can determine whether the portfolio lasts or runs out.

The message is clear: higher withdrawal rates tend to exhaust a portfolio sooner, while lower rates can extend its life. In this example, withdrawing 7% or 8% caused the portfolio to run out of money before age 85. In contrast, the 4% and 5% withdrawal rates helped the portfolio weather market declines. The 4% strategy not only preserved the portfolio but grew it over 20 years, showing how compounding can work even during retirement.

No strategy can eliminate market risk, but a smaller withdrawal rate can extend the portfolio’s life and reduce the risk of outliving your savings. Taking a more conservative withdrawal approach in the early years of retirement gives your portfolio time to recover from short-term losses and grow with the market.

A thoughtful withdrawal strategy is an important part of retirement planning. It’s not just about how much you’ve accumulated, but how you manage it. There’s no one-size-fits-all approach, and the method you start with doesn’t have to be permanent. Fixed withdrawal rates can provide a good starting point, but many retirees may benefit from more flexible approaches. For example, you could adjust withdrawals based on market conditions, taking smaller distributions in down years and larger ones in strong years.

Another option is the bucket strategy, which divides assets into short-, intermediate-, and long-term segments. By keeping 1-2 years’ worth of expenses in cash or short-term investments, you can avoid selling stocks during major market declines, such as those in 2008 or 2020. This gives long-term investments time to recover and can help create a steadier income stream over time.

Everyone’s retirement looks different. Our goal is to help you create a withdrawal strategy tailored to your unique needs and goals when that time comes.

Disclosure

The information and opinions provided herein are provided as general market commentary only – not financial advice – and are subject to change at any time without notice. This commentary may contain forward-looking statements that are subject to various risks and uncertainties. None of the events or outcomes mentioned here may come to pass, and actual results may differ materially from those expressed or implied in these statements. No mention of a particular security, index, or other instrument in this report constitutes a recommendation to buy, sell, or hold that or any other security, nor does it constitute an opinion on the suitability of any security or index. The report is strictly an informational publication and has been prepared without regard to the particular investments and circumstances of the recipient.

Past performance does not guarantee or indicate future results. Any index performance mentioned is for illustrative purposes only and does not reflect any management fees, transaction costs, or expenses. Indexes are unmanaged, and one cannot invest directly in an index. Index performance does not represent the actual performance that would be achieved by investing in a fund.

See Full Disclosures Page

Concerns or questions about how your investment portfolio will hold up in the current market environment? Contact Financial Synergies today.

We are a boutique, financial advisory and total wealth management firm with over 35 years helping clients navigate turbulent markets. To learn more about our approach to investment management please reach out to us. One of our seasoned advisors would be happy to help you build a custom financial plan to help ensure you accomplish your financial goals and objectives. Schedule a conversation with us today.

More relevant articles by Financial Synergies:

Blog Disclosures

This content, which may contain security-related opinions and/or information, is provided for informational purposes only and should not be relied upon in any manner as professional advice, or an endorsement of any practices, products or services. There can be no guarantees or assurances that the views expressed here will be applicable for any particular facts or circumstances, and should not be relied upon in any manner. You should consult your own financial advisors as to legal, business, tax, and other related matters concerning any investment.

The commentary in this “post” (including any related blogs, videos, and social media) reflects the personal opinions, viewpoints, and analyses of the Financial Synergies Wealth Advisors, Inc. employees providing such comments, and should not be regarded as the views of Financial Synergies Wealth Advisors, Inc. or its respective affiliates or as a description of advisory services provided by Financial Synergies Wealth Advisors, Inc. or performance returns of any Financial Synergies Wealth Advisors, Inc. client.

Any opinions expressed herein do not constitute or imply endorsement, sponsorship, or recommendation by Financial Synergies Wealth Advisors, Inc. or its employees. The views reflected in the commentary are subject to change at any time without notice.

Nothing on this website or Blog constitutes investment or financial planning advice, performance data or any recommendation that any particular security, portfolio of securities, transaction or investment strategy is suitable for any specific person. It also should not be construed as an offer soliciting the purchase or sale of any security mentioned. Nor should it be construed as an offer to provide investment advisory services by Financial Synergies Wealth Advisors, Inc.

Any mention of a particular security and related performance data is not a recommendation to buy or sell that security. Financial Synergies Wealth Advisors, Inc. manages its clients’ accounts using a variety of investment techniques and strategies, which are not necessarily discussed in the commentary. Investments in securities involve the risk of loss. Past performance is no guarantee of future results.

Any charts provided here or on any related Financial Synergies Wealth Advisors, Inc. personnel content outlets are for informational purposes only, and should also not be relied upon when making any investment decision. Any indices referenced for comparison are unmanaged and cannot be invested into directly. As always please remember investing involves risk and possible loss of principal capital; please seek advice from a licensed professional. Any projections, estimates, forecasts, targets, prospects and/or opinions expressed in these materials are subject to change without notice and may differ or be contrary to opinions expressed by others. Information in charts have been obtained from third-party sources and data, and may include those from portfolio securities of funds managed by Financial Synergies Wealth Advisors, Inc. While taken from sources believed to be reliable, Financial Synergies Wealth Advisors, Inc. has not independently verified such information and makes no representations about the enduring accuracy of the information or its appropriateness for a given situation. All content speaks only as of the date indicated.

Financial Synergies Wealth Advisors, Inc. is a registered investment adviser. Advisory services are only offered to clients or prospective clients where Financial Synergies Wealth Advisors, Inc. and its representatives are properly licensed or exempt from licensure. Investments in securities involve the risk of loss. Past performance is no guarantee of future results.

See Full Disclosures Page Here

Recent Posts

Weekly Market Recap | Nov. 21, 2025

Chart of the Month | S&P 500 Sets More Than 35 New Highs for Second Consecutive Year

Using Structured Notes for Enhanced Income, Protection, and Better Planning

Subscribe to Our Blog

Shareholder | Chief Investment Officer