With all of the market-moving events of the past few years – from the global pandemic to trade wars and more – it’s understandable that some investors may prefer the safety of cash. After all, a great deal of investing is behavioral and requires being comfortable with a certain level of risk. Portfolio returns are important but so is being able to sleep well at night.

And don’t get me wrong – I’m not knocking cash as an asset class. Everyone on the planet should hold some level of cash. At a minimum, probably six to twelve months worth of cash is prudent to have in an emergency fund. And it can vary from person-to-person based on factors like stability of employment, upcoming purchases, etc.

However, for those saving and investing to achieve financial goals, shifting a portfolio to cash may provide short-term comfort but will jeopardize long-term gains. In other words, it simply doesn’t strike the right balance. Finding this balance, while resisting the urge to react to short-term market developments, is one of the biggest challenges we all face. There are three reasons why this is more important than ever.

First, cash still generates little to no income and hinders portfolio growth. This has been true since the 2008 financial crisis when interest rates fell to historic lows. Nearly 12 years later, rates are still at these levels with the federal funds rate back to zero. While this is good for borrowers – the average 30-year mortgage rate is around 3% – it hurts savers and those who rely on their savings for income.

Second, not only are interest rates low, but inflation slowly erodes the value of cash. This means that, left unchecked, the purchasing power of investors’ hard-earned cash might actually decline each year. This has been true even though inflation, at least the way it’s measured by economists, has been quite low by historical standards. But even minimal inflation can have a corrosive effect when cash generates limited income, acting as a drag on overall portfolios.

Another way to describe this effect is that investors often seek safety in all the wrong places. The cash balance on a bank statement may feel safe since it is stable. However, what matters isn’t the dollar amount of cash but what it can purchase. Inflation means that the same number of dollars can purchase fewer goods and services each year. Thus, it takes actual portfolio growth to keep an investor’s purchasing power at par, let alone to create real wealth.

Finally, and most importantly, there are better ways to manage portfolio risk and increase investor comfort. After all, this is usually the reason investors seek a shift to cash in the first place: as a market-timing tool in response to short-term events.

Unfortunately, this often backfires. Not only do markets have a history of recovering when investors least expect it (the current market environment is a prime example), but diversification provides a better way to lower risk while maintaining growth. While there is simplicity in holding cash, having the right mix of stocks, bonds, and other assets can achieve a better ratio of risk and reward over long periods of time.

Ultimately, cash is an important part of any portfolio in moderation. Having the discipline to save enough in the first place is a laudable achievement. Staying invested with the right portfolio to grow this wealth also requires discipline.

Below are three charts that put the value of cash in perspective.

1. Cash still generates little to no income

Twelve years after the global financial crisis, interest rates are still near historic lows. In fact, the federal funds rate is back to the zero-lower-bound due to the COVID-19 crisis. Investors who rely on income from their cash savings may continue to find it difficult to do so without other assets.

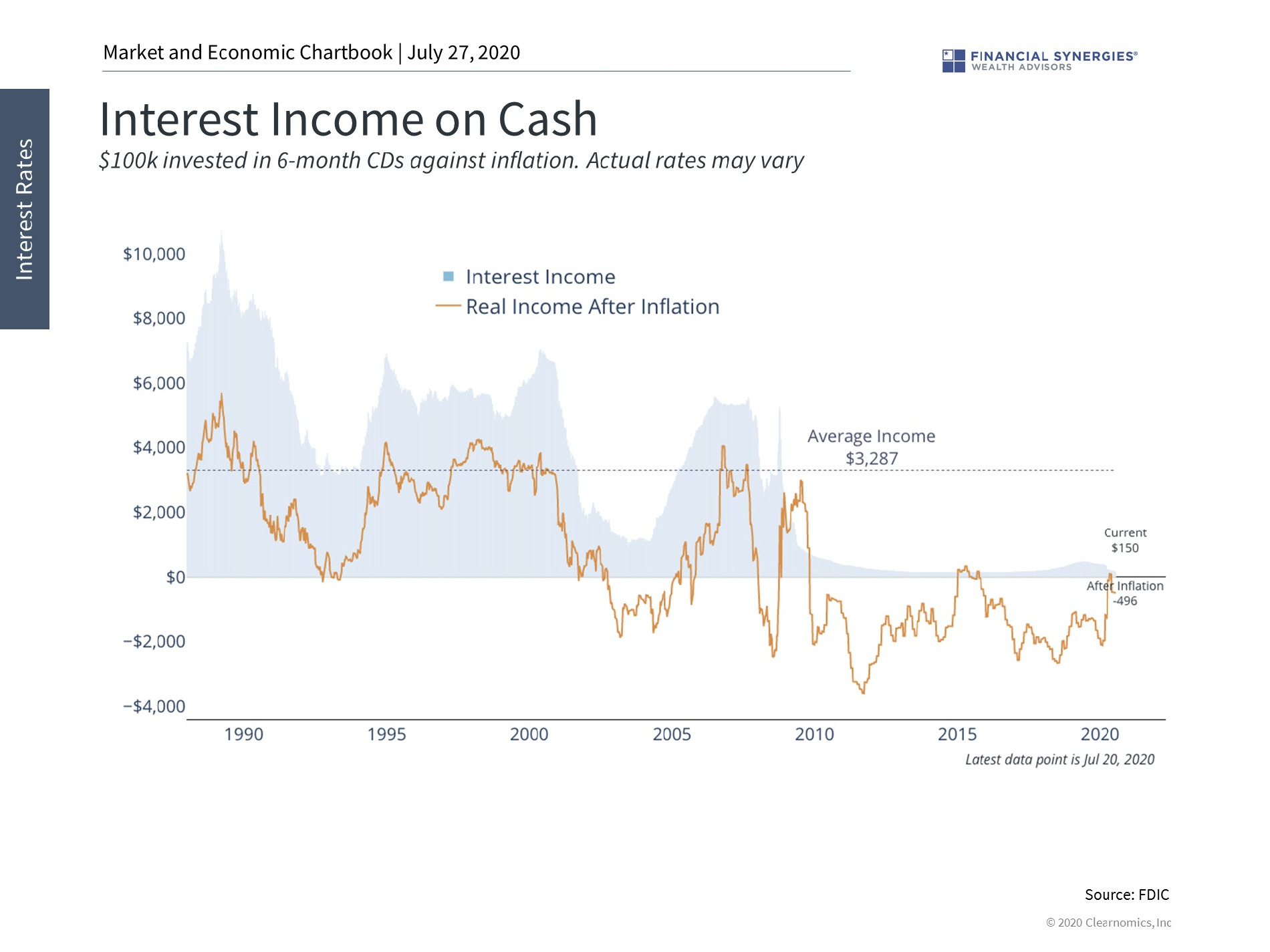

2. To make matters worse, inflation erodes the value of cash

Inflation – even at very low levels – chips away at the purchasing power of cash savings. For most of the past decade, inflation has meant that the “real” value of cash has declined each year. Although cash may feel safe, it has been anything but in this low-rate environment.

3. A portfolio approach to income and risk management is often superior

Rather than simply relying on cash, holding an appropriately-constructed portfolio can often achieve a better risk/reward ratio while maintaining growth. The key ingredient is time: investors seeking to achieve their financial goals over the long run have historically done well by staying disciplined and holding a mix of assets.

While cash is tempting, it does little to help investors when interest rates are low, inflation eats away at its value, and there are better options.

Source: Clearnomics

Cash Is Comfortable, But Can Be Counterproductive

With all of the market-moving events of the past few years – from the global pandemic to trade wars and more – it’s understandable that some investors may prefer the safety of cash. After all, a great deal of investing is behavioral and requires being comfortable with a certain level of risk. Portfolio returns are important but so is being able to sleep well at night.

And don’t get me wrong – I’m not knocking cash as an asset class. Everyone on the planet should hold some level of cash. At a minimum, probably six to twelve months worth of cash is prudent to have in an emergency fund. And it can vary from person-to-person based on factors like stability of employment, upcoming purchases, etc.

However, for those saving and investing to achieve financial goals, shifting a portfolio to cash may provide short-term comfort but will jeopardize long-term gains. In other words, it simply doesn’t strike the right balance. Finding this balance, while resisting the urge to react to short-term market developments, is one of the biggest challenges we all face. There are three reasons why this is more important than ever.

First, cash still generates little to no income and hinders portfolio growth. This has been true since the 2008 financial crisis when interest rates fell to historic lows. Nearly 12 years later, rates are still at these levels with the federal funds rate back to zero. While this is good for borrowers – the average 30-year mortgage rate is around 3% – it hurts savers and those who rely on their savings for income.

Second, not only are interest rates low, but inflation slowly erodes the value of cash. This means that, left unchecked, the purchasing power of investors’ hard-earned cash might actually decline each year. This has been true even though inflation, at least the way it’s measured by economists, has been quite low by historical standards. But even minimal inflation can have a corrosive effect when cash generates limited income, acting as a drag on overall portfolios.

Another way to describe this effect is that investors often seek safety in all the wrong places. The cash balance on a bank statement may feel safe since it is stable. However, what matters isn’t the dollar amount of cash but what it can purchase. Inflation means that the same number of dollars can purchase fewer goods and services each year. Thus, it takes actual portfolio growth to keep an investor’s purchasing power at par, let alone to create real wealth.

Finally, and most importantly, there are better ways to manage portfolio risk and increase investor comfort. After all, this is usually the reason investors seek a shift to cash in the first place: as a market-timing tool in response to short-term events.

Unfortunately, this often backfires. Not only do markets have a history of recovering when investors least expect it (the current market environment is a prime example), but diversification provides a better way to lower risk while maintaining growth. While there is simplicity in holding cash, having the right mix of stocks, bonds, and other assets can achieve a better ratio of risk and reward over long periods of time.

Ultimately, cash is an important part of any portfolio in moderation. Having the discipline to save enough in the first place is a laudable achievement. Staying invested with the right portfolio to grow this wealth also requires discipline.

Below are three charts that put the value of cash in perspective.

1. Cash still generates little to no income

Twelve years after the global financial crisis, interest rates are still near historic lows. In fact, the federal funds rate is back to the zero-lower-bound due to the COVID-19 crisis. Investors who rely on income from their cash savings may continue to find it difficult to do so without other assets.

2. To make matters worse, inflation erodes the value of cash

Inflation – even at very low levels – chips away at the purchasing power of cash savings. For most of the past decade, inflation has meant that the “real” value of cash has declined each year. Although cash may feel safe, it has been anything but in this low-rate environment.

3. A portfolio approach to income and risk management is often superior

Rather than simply relying on cash, holding an appropriately-constructed portfolio can often achieve a better risk/reward ratio while maintaining growth. The key ingredient is time: investors seeking to achieve their financial goals over the long run have historically done well by staying disciplined and holding a mix of assets.

While cash is tempting, it does little to help investors when interest rates are low, inflation eats away at its value, and there are better options.

Source: Clearnomics

Recent Posts

2nd Quarter 2025 Market and Economic Review

The Market Reaches All-Time Highs

Last Week on Wall Street: Broad-Based Market Rally [June 30-2025]

Subscribe to Our Blog

Shareholder | Chief Investment Officer