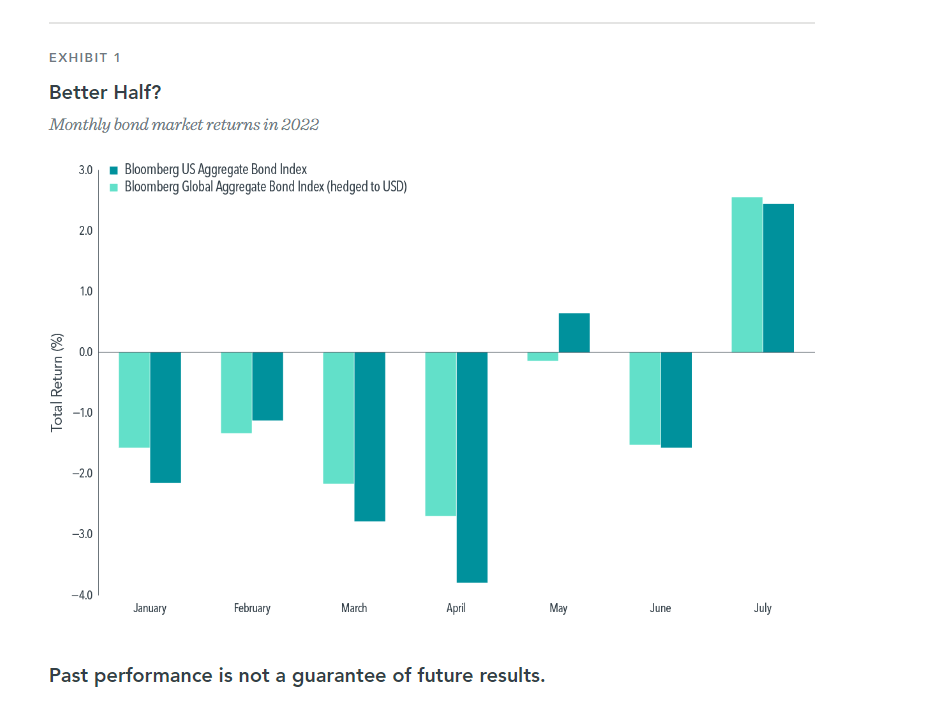

Despite the first two quarters of 2022 bringing the worst US bond market returns since 1980,1 July delivered a positive beginning for bonds in the third quarter. For the month of July, the US bond market returned 2.44%, while the global bond market returned 2.55% (see Exhibit 1).

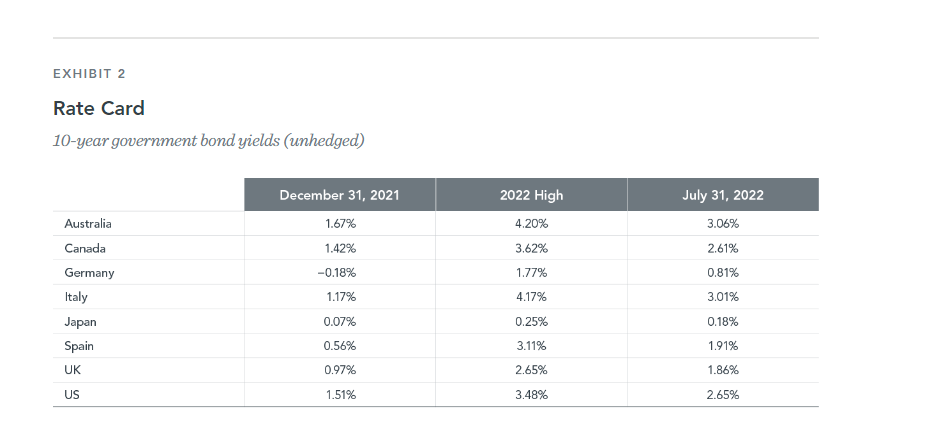

Even though US interest rates increased significantly during the first two quarters, they have quietly decreased from their highs earlier this year. The yield on the 10-year US Treasury note peaked at 3.48% in June and then decreased to 2.65% by the end of July. Interest rates in the global developed markets have also generally decreased from their 2022 highs (see Exhibit 2). However, bond yields are still elevated relative to the start of the year, contributing to higher expected returns for bond investors.

Investors who recently shortened the duration (too aggressively) of their fixed income allocation because they were expecting a continuation of higher interest rates may have missed the positive term premium in July. For the month of July, short-term US government bonds returned 0.42% while the broad US government bond market returned 1.58%. Outside the US, short-term government bonds returned 0.69%, while the broad government bond market returned 3.11%.2

Turning to credit, US credit spreads widened during the first two quarters of the year, resulting in corporate bonds underperforming government bonds. For example, US credit spreads began the year at 87 basis points3 and widened to 148 basis points by early July, before stabilizing for the remainder of the month. A widening of credit spreads is not a reason to abandon corporate bonds. In fact, wider credit spreads indicate larger expected credit premiums.

It should be intuitive—higher yields on corporate bonds relative to government bonds tend to signal higher expected returns for corporate bonds relative to government bonds. And, indeed, credit premiums were also positive in July with corporate bonds outperforming government bonds. For instance, US intermediate-term corporate bonds returned 2.37%, while US intermediate-term government bonds returned 1.33%.4 Globally, intermediate-term corporate bonds returned 2.71%, while intermediate-term government bonds returned 1.19%.5

The first seven months of 2022 highlight how difficult it is to predict the future path of interest rates. They increased significantly for the first six months of the year and then decreased. Credit spreads widened, then stabilized. Furthermore, the positive term and credit premiums generated in July illustrate the importance of remaining disciplined and diversified, with a focus on the appropriate asset allocation, to achieve long-term goals.

Source: Dimensional Fund Advisors

FOOTNOTES

1Bloomberg US Aggregate Bond Index.

2Bloomberg US Government Bond Index 1-3 Years, Bloomberg US Government Bond Index, FTSE World Government Bond Index ex-US 1-3 Years (hedged to USD), and FTSE World Government Bond Index ex-US (hedged to USD). FTSE fixed income indices © 2022 FTSE Fixed Income LLC. All rights reserved.

3Bloomberg US Credit Bond Index Option Adjusted Spread.

4Bloomberg US Intermediate Government and Corporate Bond Indices.

5Bloomberg Global Intermediate Government and Corporate Bond Indices.

Bonds Get Positive

Despite the first two quarters of 2022 bringing the worst US bond market returns since 1980,1 July delivered a positive beginning for bonds in the third quarter. For the month of July, the US bond market returned 2.44%, while the global bond market returned 2.55% (see Exhibit 1).

Even though US interest rates increased significantly during the first two quarters, they have quietly decreased from their highs earlier this year. The yield on the 10-year US Treasury note peaked at 3.48% in June and then decreased to 2.65% by the end of July. Interest rates in the global developed markets have also generally decreased from their 2022 highs (see Exhibit 2). However, bond yields are still elevated relative to the start of the year, contributing to higher expected returns for bond investors.

Investors who recently shortened the duration (too aggressively) of their fixed income allocation because they were expecting a continuation of higher interest rates may have missed the positive term premium in July. For the month of July, short-term US government bonds returned 0.42% while the broad US government bond market returned 1.58%. Outside the US, short-term government bonds returned 0.69%, while the broad government bond market returned 3.11%.2

Turning to credit, US credit spreads widened during the first two quarters of the year, resulting in corporate bonds underperforming government bonds. For example, US credit spreads began the year at 87 basis points3 and widened to 148 basis points by early July, before stabilizing for the remainder of the month. A widening of credit spreads is not a reason to abandon corporate bonds. In fact, wider credit spreads indicate larger expected credit premiums.

It should be intuitive—higher yields on corporate bonds relative to government bonds tend to signal higher expected returns for corporate bonds relative to government bonds. And, indeed, credit premiums were also positive in July with corporate bonds outperforming government bonds. For instance, US intermediate-term corporate bonds returned 2.37%, while US intermediate-term government bonds returned 1.33%.4 Globally, intermediate-term corporate bonds returned 2.71%, while intermediate-term government bonds returned 1.19%.5

The first seven months of 2022 highlight how difficult it is to predict the future path of interest rates. They increased significantly for the first six months of the year and then decreased. Credit spreads widened, then stabilized. Furthermore, the positive term and credit premiums generated in July illustrate the importance of remaining disciplined and diversified, with a focus on the appropriate asset allocation, to achieve long-term goals.

Source: Dimensional Fund Advisors

FOOTNOTES

1Bloomberg US Aggregate Bond Index.

2Bloomberg US Government Bond Index 1-3 Years, Bloomberg US Government Bond Index, FTSE World Government Bond Index ex-US 1-3 Years (hedged to USD), and FTSE World Government Bond Index ex-US (hedged to USD). FTSE fixed income indices © 2022 FTSE Fixed Income LLC. All rights reserved.

3Bloomberg US Credit Bond Index Option Adjusted Spread.

4Bloomberg US Intermediate Government and Corporate Bond Indices.

5Bloomberg Global Intermediate Government and Corporate Bond Indices.

Recent Posts

Should You Fear Market All-Time Highs?

Last Week on Wall Street: Trade and Jobs Cheer Markets [July 7-2025]

2nd Quarter 2025 Market and Economic Review

Subscribe to Our Blog

Shareholder | Chief Investment Officer