4 Avoidable Financial Errors for Millennials & Gen X

First off, lets clarify any confusion between the terms Gen X and Millennials. Generation X is currently age 40 to 54 (born between 1965 and 1979). Millennials (also known as Generation Y) are currently age 24 to 39 (born between 1980 and 1995).The most common misconception is only thinking of Millennials as “college-age” adults. The largest cohort on college campuses today is Generation Z – born between 1995 & today.

1. Risk-Aversion After “The Great Recession”

Whether at that time you were entering your prime earning years or just beginning to have an awareness of the economy, The Great Recession of 2008-2009 had a lasting impact on all of us. However, we cannot allow this fear of investing to drive our financial decisions throughout our career or we will never achieve true financial independence.

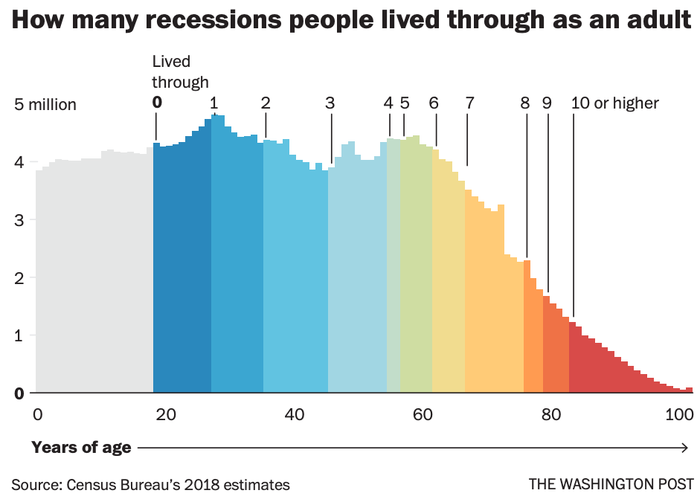

As unpleasant as recessions are, they are normal. Refer to the graph above, which illustrates the number of recessions Americans have experienced based on current age. Not only have current retirees experienced 5 to 10+ recessions over their adult lifetime, but they also INVESTED through 5 to 10 recessions.

As unpleasant as recessions are, they are normal. Refer to the graph above, which illustrates the number of recessions Americans have experienced based on current age. Not only have current retirees experienced 5 to 10+ recessions over their adult lifetime, but they also INVESTED through 5 to 10 recessions.

Researchers estimate current retirees have accumulated more than $30 TRILLION in investable assets (a ‘TR’, not a ‘B’ as in Billion but a ‘TR’). Now that’s a big number – ($30,000,000,000,000) twelve zeros after the first comma! This makes them the wealthiest generation in history. This great feat was not achieved by fear of the markets or attempting to time the market. It took consistent and continuous saving and investing for their future, AND guess what? It worked!

At this point, annual returns are not a primary concern for wealth accumulators. Given we still have DECADES before we will need to rely on our portfolios to generate an income for us. The primary concern we, as accumulators, would have if a recession hits is losing our jobs. Not the fact that our portfolio temporarily decreases in value.

2. (Attempting To) “Time the Market”

Okay, so what is timing the market (or market timing)? Market timing basically means shifting your investments in and out of cash based on short-term market speculation (sound dangerous?). STEP 1: Sell all your investments to lock-in market gains prior to the market experiencing a decline. STEP 2: Reinvest your cash prior to the market increasing in value. Essentially, only participating in the market while it is increasing in value.

Who wouldn’t want to implement a strategy that avoids participating in declining markets? Does this sound too good to be true? Well, that’s because it is. In order to implement an effective market timing strategy, you must get BOTH calls right every single time.

In reality, there are two types of investors: Investors who KNOW they don’t know where the market is going in the short-run, and Investors who DON’T KNOW they don’t know where the market is going in the short-run. This is a major risk for wealth accumulators as it is impossible to consistently make these calls.

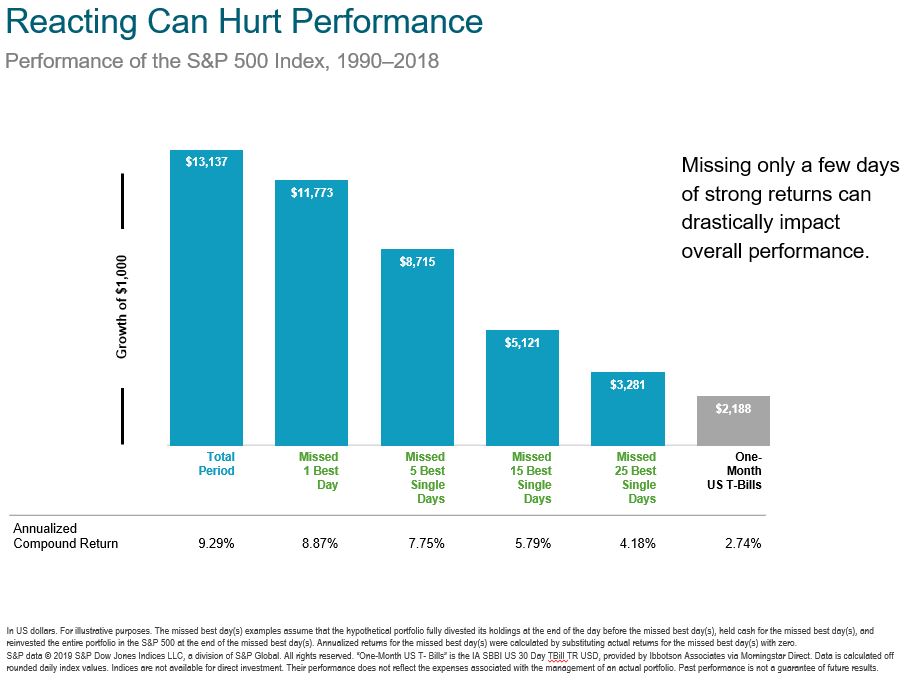

Over the past 28-years (1990 through 2018), if you were fully invested in the S&P 500 for the entirety, you would have averaged 9.29%. While missing ONLY the 25 BEST DAYS over this 28-year period, you might as well have kept your money in cash (illustrated as one-month Treasury Bills). The reason being, you took on substantially more risk to receive an underwhelming additional 1.44% annually rather than simply keeping your money in cash.

Over the past 28-years (1990 through 2018), if you were fully invested in the S&P 500 for the entirety, you would have averaged 9.29%. While missing ONLY the 25 BEST DAYS over this 28-year period, you might as well have kept your money in cash (illustrated as one-month Treasury Bills). The reason being, you took on substantially more risk to receive an underwhelming additional 1.44% annually rather than simply keeping your money in cash.

Market Timing may sound good, but in practice it is impossible to replicate this time and time again. Simply because it is impossible to predict when the recovery will happen. Market declines and market recoveries tend to take place in very tight windows. The most important thing for accumulators is time-in-the-market, not market timing.

3. Not Automating Your Savings

If you thought finances and investing were emotional before, just wait until you try to determine a specific time to invest a large sum of cash, which you have been sitting on awaiting the ‘perfect’ opportunity to invest these dollars.

Not automating your savings based on the fear of short-term volatility is one of the most dangerous risks of all for accumulators (and probably the one I see the most often). The reason being the silent killer called INFLATION.

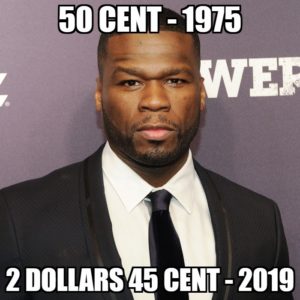

You may know Curtis James Jackson III, aka 50 Cent. Well, Mr. Jackson was born in 1975 – fast forward 44 years to today (is 50 Cent REALLY 44?!). Anyway, over this time period the United States has experienced an average annual inflation rate of 3.68% (including the hyper-inflationary period of the 1970s and early 80s). In order to have the same purchasing power today of $0.50 in 1975, you would need $2.45 today. This may not seem like a huge difference when starting with such a small dollar amount, so let’s raise the ante a bit. Let’s take a $500,000 portfolio in 1975 and fast forward once again to today. To have the same purchasing power today, you would need to have a portfolio of $2,452,163.93… almost five times more money than in 1975!

You may know Curtis James Jackson III, aka 50 Cent. Well, Mr. Jackson was born in 1975 – fast forward 44 years to today (is 50 Cent REALLY 44?!). Anyway, over this time period the United States has experienced an average annual inflation rate of 3.68% (including the hyper-inflationary period of the 1970s and early 80s). In order to have the same purchasing power today of $0.50 in 1975, you would need $2.45 today. This may not seem like a huge difference when starting with such a small dollar amount, so let’s raise the ante a bit. Let’s take a $500,000 portfolio in 1975 and fast forward once again to today. To have the same purchasing power today, you would need to have a portfolio of $2,452,163.93… almost five times more money than in 1975!

I am by no means saying that automating your investing will stop inflation, but it will give you the best chance of growing your wealth for yourself and your family at a rate that will outpace inflation over the long-run. It is critical to automate savings as soon as possible. Even if you are starting with a small amount, you must start somewhere. Automate your savings now so it becomes a habit later.

4. Not Contributing to Employer Retirement Plans

Employer retirement plans include 401(k)s, 403(b)s, SIMPLE IRAs, Thrift Savings Plans, etc. In almost all cases, at a minimum, you should contribute enough to receive the full employer match. For example, let’s use the basic safe harbor 401(k). If an employee contributes 5% to their personal 401(k), then the employer will match 100% of the first 3% the employee contributes, PLUS 50% of the next 2% the employee contributes. All said and done, you the employee contributes 5% and the employer contributes 4%, so a total of 9% is going into your personal 401(k). This is a guaranteed 80% return on your money just by contributing to the plan. How could anyone pass that up? Guarantees aren’t common in investing so don’t let this one pass you by!

Conclusion

As accumulators, we must avoid all these mistakes to give us the best chance of long-term financial stability and success. Staying disciplined, working through the high high’s and low low’s we are all going to experience through our working careers is something we must strive for. After all, a short-term reduction in market prices allows us to purchase a greater quantity of shares with the same dollar amount – allowing us to participate more when the market inevitably increases in value.

Finances are likely in the top 2-3 concerns anyone has, so sticking to a plan and staying disciplined can be difficult. When it comes to financial affairs, keeping your emotions in check is absolutely critical to your long-term success. In the event you need assistance in this arena, Financial Synergies Pathway® was built with you in mind. To schedule a free, no-obligation consultation please reach out to us. We would be glad to act as a resource for you, as you determine the best path forward for you and your family.

Sources:

https://www.cnbc.com/2018/05/22/that-30-trillion-great-wealth-transfer-is-a-myth.html